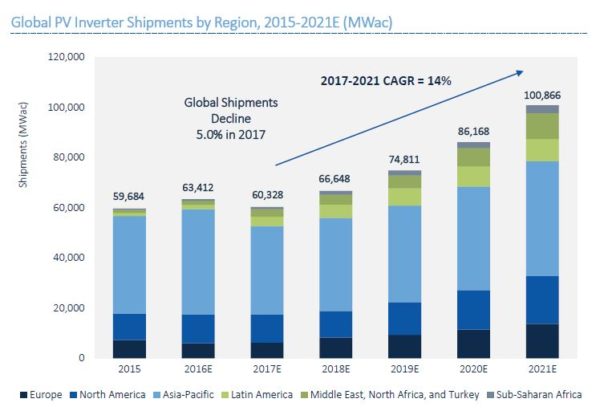

The global PV inverter industry will record a 5% contraction in shipments next year as the markets of China, the U.S. and Japan decline, finds the latest Global PV Inverter and MLPE H1 2016 Report by GTM Research.

Total inverter shipments are set to reach a record 63.5 GWac this year, up from 59.7 GWac in 2015, but will fall to 60.3 GWac in 2017 as the market takes a breather. However, GTM Research forecasts steady growth from 2018 onwards, with shipments growing to 66.6 GWac that year, then rising steadily towards more than 100 GWac by 2021.

As the market grows, the number of leading players has consolidated. GTM Research finds that the ten largest suppliers of solar inverter will this year meet 80% of demand, led by Huawei, Sungrow and SMA in terms of shipments. “We haven’t seen the leading vendors hold share this high since 2010, when solar demand was highly centered in continental Europe,” said report author and GTM Research senior solar analyst Scott Moskowitz.

China’s Huawei – which edged out Germany’s SMA to top the shipments chart in 2015 – has retained first place for shipments with 17% of market share in the first half of the year, followed by Sungrow (China), SMA, Sineng (China), TMEIC (Japan), TBEA Sunoasis (China), ABB (Switzerland), KStar (China), General Electric (U.S.) and SolarEdge (Israel).

However, given China’s H1, pre FIT-cut installation rush and subsequent H2 slowdown, the final year picture could well look quite different once all data are in.

The Chinese market makes up 90% of Huawei’s and Sungrow’s sales, while a dominance of the higher price U.S. market has helped SMA once again generate the most revenue from sales this year in a global market worth an estimated $3.2 billion. Huawei snapped up second-place in terms of revenue, followed by TMEIC, SolarEdge, ABB, Sungrow, Schneider Electric (France), Enphase Energy (U.S.), Omron (Japan), Fronius (Austria), Sineng and General Electric.

Distinct trends

As price pressures continue to bite, GTM Research expects further M&A activity in 2017, citing this year’s acquisition of Bonfiglioli by Spain’s Ingeteam as a sign of things to come as firms look to accelerate global expansion.

Huawei is poised to shape the industry further in 2017 with its expected entrance into the residential market with a new power optimizer/microinverter product. This, GTM Research believes, will exert greater price pressure on all residential inverter solutions, and will mirror the trend that has seen central inverter prices fall 10% since H1 2016 in response to the Huawei-driven trend for installing string inverters at scale.

“Pricing pressure remains a constant, unrelenting reality in the maturing solar inverter market,” said Moskowitz. “Central inverter prices in the U.S. have fallen the most half-over-half due to increased competition from string and the proliferation of lower cost, 1,500 volt models.”

The wider adoption of 1,500 volt inverters makes these inverters some 10% cheaper than 1,000 volt inverters thanks to higher power densities, thus facilitating further growth of these higher voltage inverters.

Despite these price pressures and a 5% shipment decrease forecast for 2017, revenue will fall by only 1.2% in 2017 as gains are made in the residential string and module level power electronics (MLPE) space.

Looking ahead, GTM Research expects China to remain the world’s largest solar market through 2021, while the Middle East and Southeast Asia regions will each enjoy CAGR of above 25% for the next five years, making them the fastest-growing markets for inverters globally.

Other trends that GTM Research will pay attention to include the opportunities that exist in maturing markets such as Europe and Japan for retrofitting old and aging inverters; the growing need for communications protocols and control capabilities for utilities and grid operators; the opportunities that exist in the growing but undefined solar+storage market, and the drive for higher power density replacing the drive for higher efficiency.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.