Author: Sophie Vorrath, for RenewEconomy

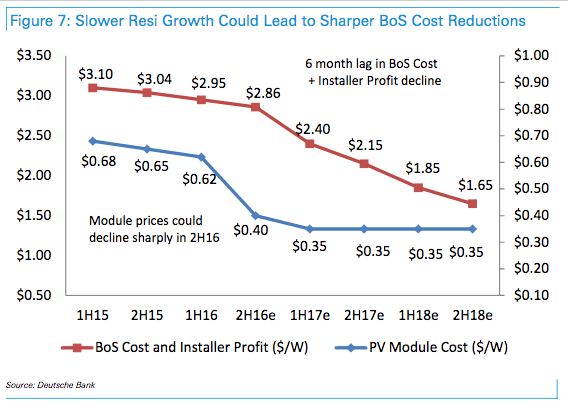

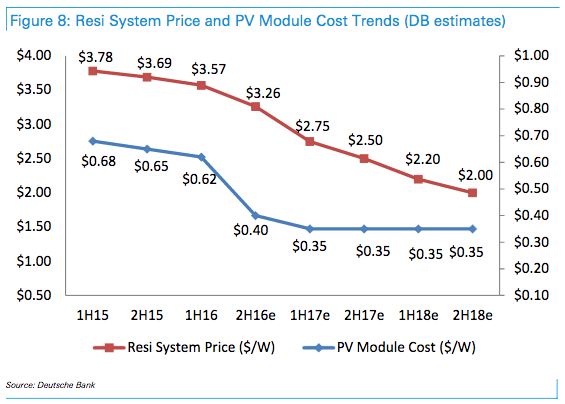

Deutsche Bank’s U.S. solar market report, published on Wednesday, predicts solar module prices will drop to $0.35 per watt in Q4 2016, having already fallen already by one-third in Q3, down from $0.60/W to $0.40.

The Q3 price drop already charted, combined with Deustche Bank’s projections for Q4, would mean a total fall in US module prices of 40% in just two quarters.

The U.S. PV market has been notable for its heavy “balance of system” costs, mostly related to the planning and approvals process. By contrast, Australian solar system prices average around AUS$1.63/W, less than half the average price for residential installation in the US.

But, as the Deutsche report illustrates, this appears to be changing – and rather rapidly.

“Average residential solar system prices in the US market have only modestly decreased from $3.86W in 2H14 to $3.57/W in 1H16. Most of the price reduction during this period was driven by BoS cost reduction,” the report says.

“However, considering the recent precipitous drop in module prices (from ~60/W to less than 40c/W), we expect system prices to decline at a much more rapid pace – in the base case scenario assuming a 6-month lag for BoS cost reductions and taking into consideration some of the recent module pricing data points, we estimate system prices of $3.26/W in 2H16, $2.75/W in 1H17, $2.5/W in 2H17 and $2/W in 2H18.”

In a more optimistic scenario, Deutsche Bank says, it estimates system prices of $3.17/W in 2H16, $2.62/W in 1H17, $2.22/W in 2H17 and ~$1.7/W in 2H18.

“This precipitous decline in module prices is also accompanied by a sharp decline in inverter prices,” the report says, “especially in the utility-scale and C&I (commercial and industrial) markets.

“As a result, we expect solar economics in several U.S. markets to improve significantly over the next 12-18 months,” Deutsche Bank says.

“We expect the final “gold rush” in the US market to begin in 2017. Our view is also supported by the strong pipeline of utility scale-solar projects – we estimate roughly 8GW of solar projects under development in Texas and 31GW in the entire US.”

For 2018-20, Deutsche forecasts strong growth in all segments, and raises its demand estimates from 13.2GW, 15.2GW and 17.4GW to 16.5GW, 18GW and 19.7GW respectively.

This article was originally published on Renew Economy. It was reproduced with permission.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.