Given that modules from the early 2010s solar boom are nearing the end of their expected lifespans, it’s no surprise that a repowering wave has seemed imminent for some time. We’ve all heard the saying: new is always better, and it seems solar buyers agree. The tsunami of mass panel retirements hasn’t crashed yet.

According to new data from secondary solar market platform EnergyBin and urban mining startup Buckstop’s 2025 PV Module Price Index – Secondary Solar Market, used and legacy modules represented just 2% of resale supply listed on EnergyBin’s wholesale market last year, down from 5% in 2024 and 9% in 2022.

While the report notes that 2022 first looked like the harbinger of a multi-year repowering trend reliant on panel decommissioning and remarketing, the used module supply on EnergyBin in the years following “failed to reflect such a trend.” 98% of modules listed on the platform last year were brand-new, never having been installed and largely originating from project cancellations or delays that leave developers with excess inventory.

In total, 1.62 million modules were listed for resale on EnergyBin in 2025, a 16.8% increase from 2020. The downstream solar hardware market is slowly but surely expanding, though the growing glut of new modules may make it harder for resale economics to pencil out.

“The global oversupply of modules has definitely resulted in a more challenging market for reuse,” explained Nick Kumleben, the co-founder and chief business development officer at Buckstop, who co-authored the report. However, he told pv magazine USA, the market seems to be improving so far in 2026, as new panel prices are likely to increase due to input cost inflation and new tariff measures.

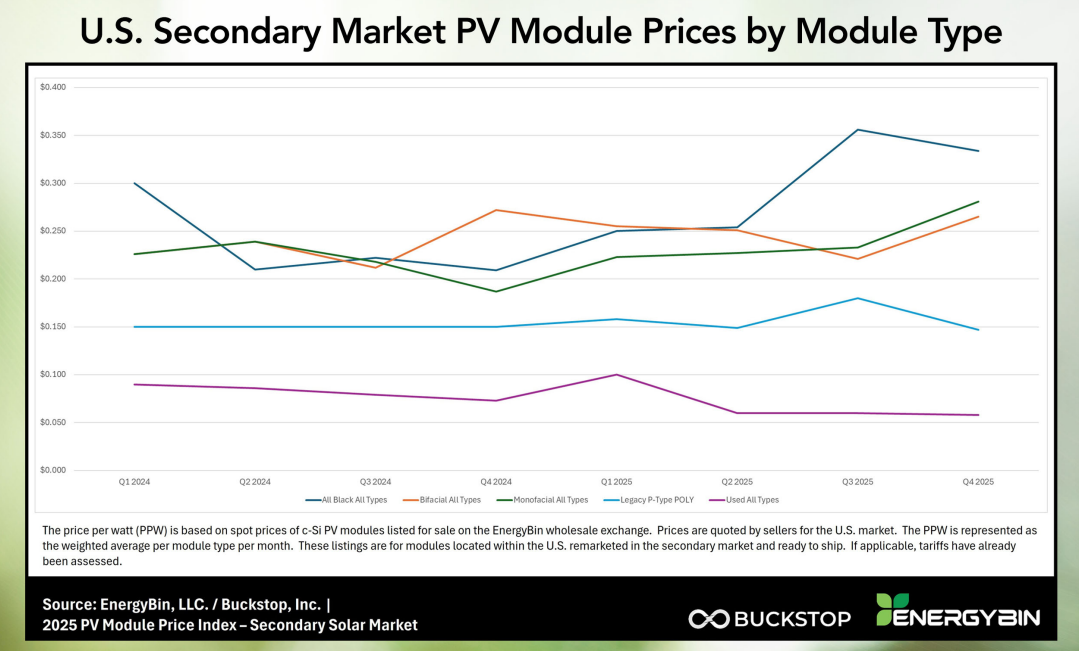

Overall, secondary market prices tend to be 20 to 70% less than primary market prices. This is particularly true for used equipment. According to the index, the average price for used modules dropped by 30% from January 2024 levels, falling to $0.058/W by the fourth quarter of 2025.

That’s a razor-thin resale margin that can make remarketing and repairs difficult, uneconomical or not worth the time and money. That could be one reason why much of today’s used module supply appears to be bypassing wholesale marketplaces altogether to be exported or recycled directly.

“The market could certainly be more transparent,” Kumleben said, especially “given the multiple trade classifications available to exporters of used panels and the sensitive nature of disposal decisions.”

The report notes that the price of used modules will likely stay below 10 cents per watt “until the world market corrects for oversupply of new modules.” But not all used models will feel the squeeze equally.

Panels less than ten years old with degradation rates below roughly 0.5% to 1% per year still retain some resale potential, particularly if they remain defect-free. Buyers are increasingly prioritizing long-term reliability, and Kumleben noted that panels with lower degradation rates have more resale opportunities later in their lifecycle.

“The race to the bottom has resulted in ample errors occurring within a few years of deployment,” the authors write, pointing toward the move from a fully tempered 3.2 mm glass to a 2.0 mm double-glass design that’s made modules more fragile.

Technology shifts also play a role, with P-type modules making up 72% of all resale inventory across black, bifacial and monofacial categories. As the market transitions more fully to N-type architectures, sellers are expected to speed up the phase-out of older technology. Per the May 2026 International Technology Roadmap for Photovoltaics (ITRPV) 16th Edition, the market share of PERC cells is expected to drop to 10% by 2027 and disappear entirely by 2035.

“Technology transitions do result in challenges for resale economics, but it’s important to remember that in most resale markets, the competition is not always from new modules,” Kumleben noted. He pointed out that often, “the alternative to a used panel is a diesel generator or no power supply at all.”

Legacy modules, too, are struggling in the resale market and accounted for a mere 1% of supply last year. While they may be new and unused, legacy panels often can’t keep pace with newer, higher-efficiency modules; resale gets impractical.

Secondary market dynamics could still shift, as declining new module prices may even out as Chinese manufacturers face sustained losses. But sharply rising silver prices, which have shot up more than 200% over the past year, are making manufacturing more expensive. Pre-owned solar could create an opportunity, the report notes.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.