The U.S. Senate released its version of the reconciliation bill, building upon the House’s draft from several weeks ago. The House version contained language restricting access to solar tax credits for entities linked to Foreign Entities of Concern (FEOC), a term widely interpreted as targeting China in the context of solar and storage technologies.

The Senate’s draft goes even further. In addition to restricting tax credits, it imposes a new 30% excise tax on solar projects if any of their manufactured components or intellectual property are determined to have originated from a FEOC, even if the project never claimed a tax credit.

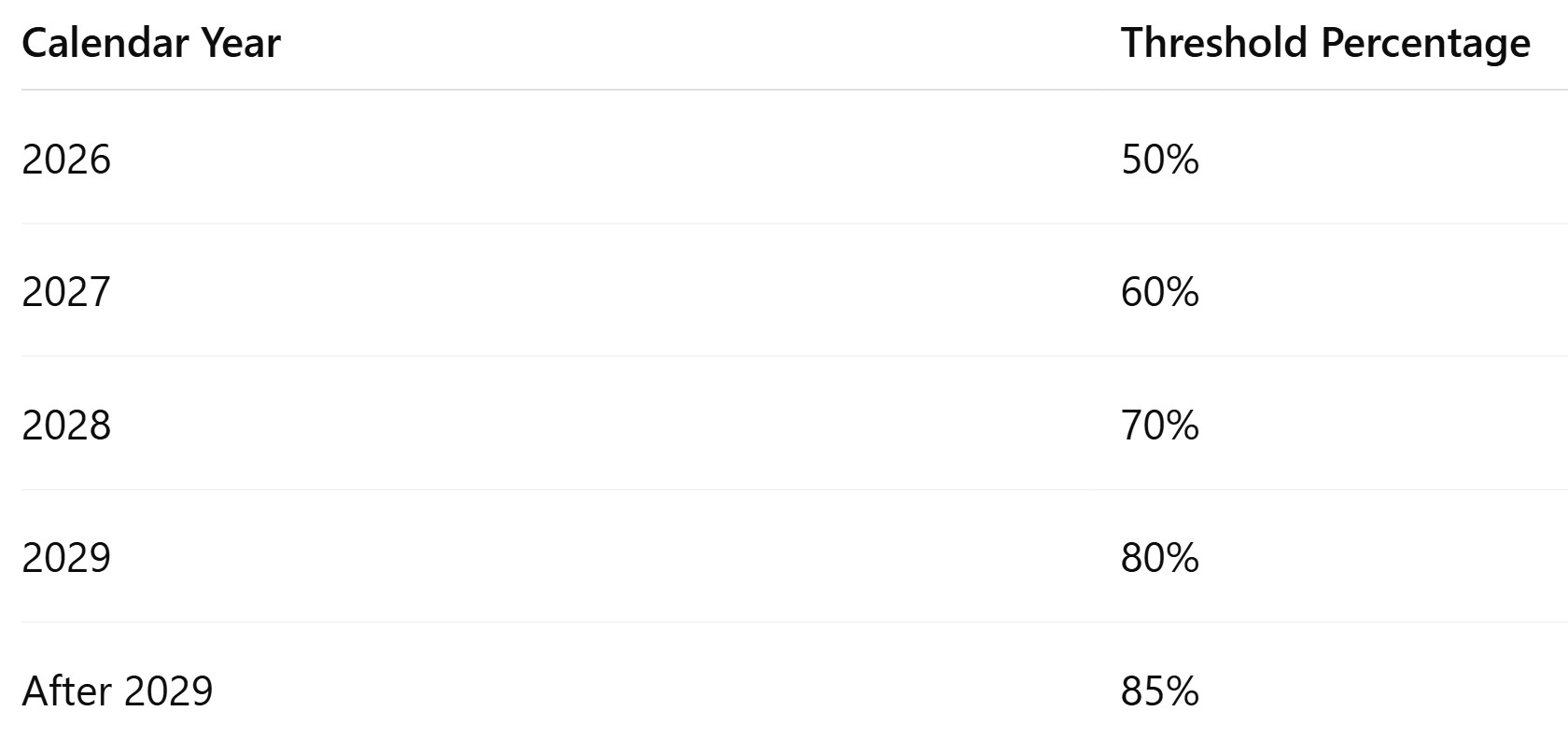

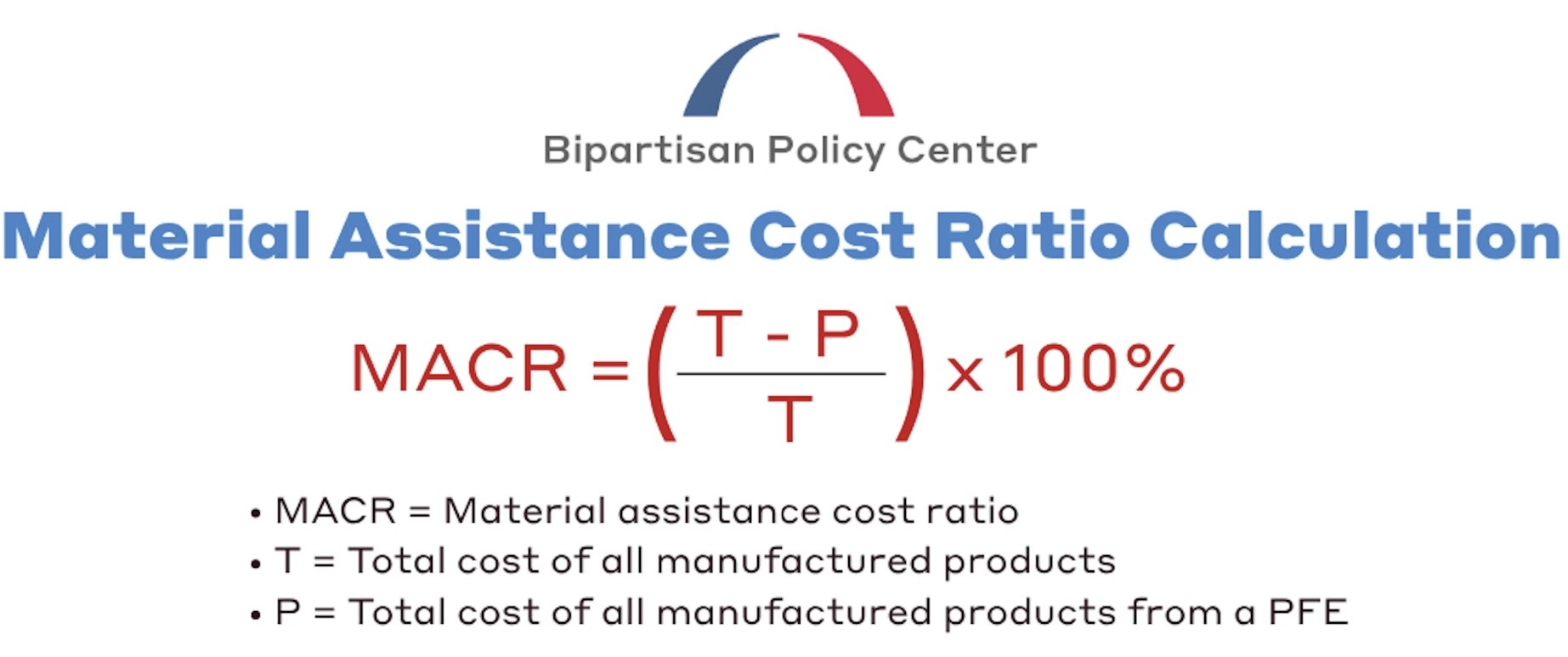

According to the draft legislation, solar projects placed in service after 2027 will be subject to the excise tax, unless construction is already underway by the signing date of the bill. A “Material Assistance Cost Ratio Calculation” would be required for each project that crosses the FEOC threshold. This compares the cost of all manufactured goods from FEOC sources to the total cost of manufactured goods in the project.

Source: Bipartisan Policy Center

The Bipartisan Policy Center outlined how the cost ratio would be calculated and published a helpful summary and chart showing how the rules might apply. Their analysis warns that poorly defined thresholds and vague enforcement guidelines could stall clean energy investment across the board.

While the Senate bill specifies a 30% excise tax, multiple interpretations have emerged about how it might be applied, according to sources contacted by pv magazine USA. Potential approaches include:

- A flat 30% tax on all manufactured goods within a project, if the project crosses the threshold.

- A scaled tax on the overage: for example, if 60% of materials are FEOC-linked and the threshold is 50%, a 10% excess would be taxed at 30%.

- A 30% tax applied only to the value of FEOC-sourced goods, if the threshold is crossed.

At press time, no formal IRS guidance has clarified which interpretation would be enforced. Regardless of the method, developers warn that the policy adds a layer of uncertainty and risk to project financing, particularly as safe harbor tables, certification rules, and contract exceptions have yet to be finalized.

According to Norton Rose Fulbright, a “specified foreign entity” is:

Any company that is owned more than 50% by the Chinese, Russian, North Korean or Iranian government, by a company organized or having its principal place of business in one of the four countries, or by CATL, Gotion, BYD, EVE Energy Company, Hithium Energy Storage Technology, companies on the OFAC list or companies that make products that benefit from Uyghur forced labor in Xinjiang in western China.

As debate over the bill intensifies, observers point out that this is one of several provisions aimed at restricting China’s role in clean energy supply chains. But critics argue the new excise tax doesn’t just penalize imported materials. It punishes the origin of ideas and creates an enforcement regime that may be impossible to navigate without chilling domestic deployment.

UPDATE: As of 11 a.m. on Tuesday, the excise tax was removed from the bill.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.