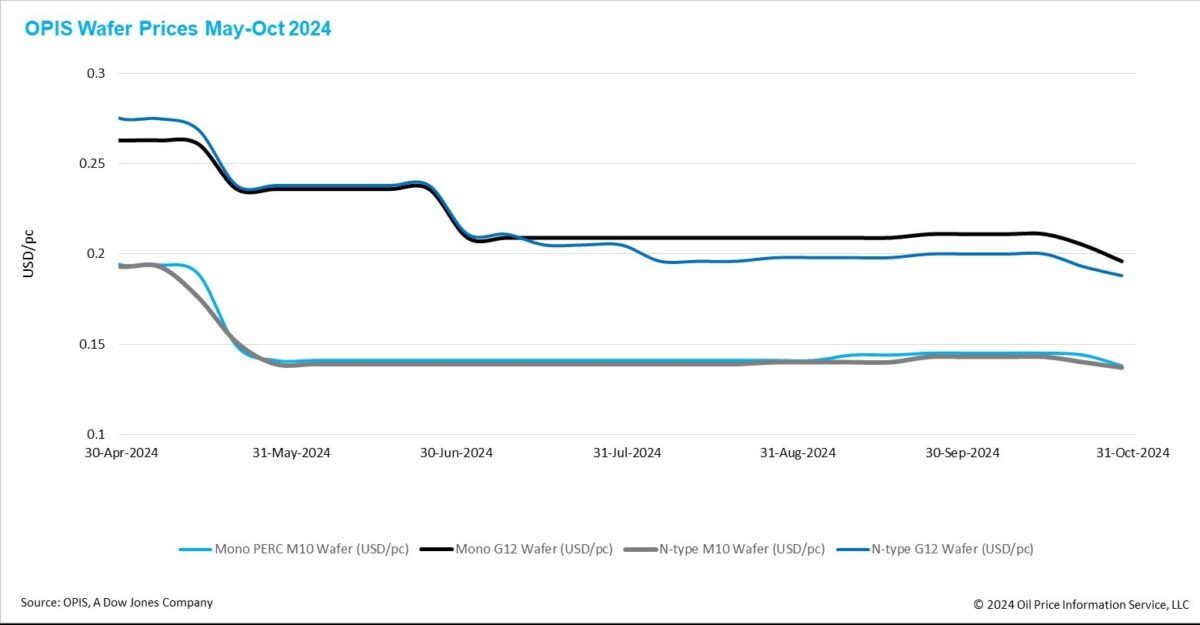

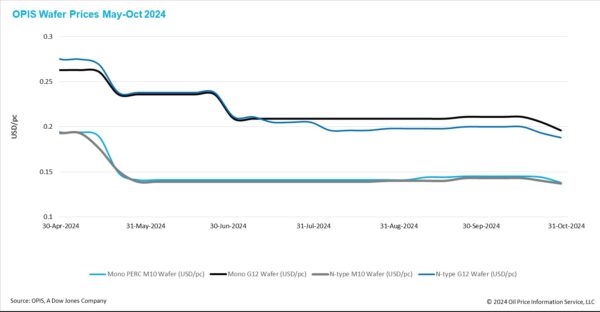

FOB China prices for wafers declined across the board for the second consecutive week. Mono PERC M10 and n-type M10 wafer prices were reported at $0.138/pc and $0.137/pc, reflecting week-to-week decreases of 4.17% and 2.14%, respectively. Similarly, Mono PERC G12 and n-type G12 wafer prices fell to $0.196/pc and $0.188/pc, marking declines of 4.39% and 2.59% compared to the previous week.

Tier-1 wafer manufacturers have been advocating for and leading price increases over the past two months despite challenging market conditions, occasionally achieving success. However, recent market developments have gradually caused them to lose control over price trends.

Sluggish downstream demand— particularly the declining demand for 182mm and 183mm wafers—has resulted in a rebound in the overall wafer inventory, now reaching 4 to 5 billion pieces, or approximately 35-40 GW. This rise suggests the cycle of clearing excess inventory in the wafer market has been extended once again, prolonging the challenging conditions in this segment.

In response, major manufacturers have initiated price cuts and inventory sales in an urgent bid to recoup funds. Sources report that some n-type M10 wafers are now available on the market for as low as CNY 1/pc ($0.124/pc), signaling a likely downward trend in wafer prices in the near future.

In the fourth quarter, wafer producers are expected to face significant strain, managing costs through wage cuts and layoffs while reducing inventory by lowering operating rates and cutting prices. A Tier-1 wafer producer, previously known for maintaining high operating rates as a core strategy, has reportedly reduced its rate to below 40%, with expectations to drop further to 30% in November—placing it even below some Tier-2 manufacturers.

Sources indicate that most wafer companies will likely see their operating rates fall to around 30% on average this quarter. Additionally, wafer producers have attracted negative attention recently due to sharp production declines. Public records show multiple court filings in October alone concerning labor disputes and compensation issues within the industry.

The U.S. market, by contrast, has seen favorable policy developments for local solar manufacturing. Last week, the U.S. Department of Treasury clarified that solar ingots and wafers qualify as semiconductor manufacturing, making them eligible for the 25% Advanced Manufacturing Investment Credit. Sources suggest this credit can be combined with other incentives, including tax credits from the Inflation Reduction Act.

Additionally, the Department of Treasury released final regulations for the 45X Advanced Manufacturing Production Tax Credit, allowing producers to claim deductions based on annual sales of eligible products. With a set rate of $12/m2 for wafers—requiring the use of U.S.-made ingots to qualify—industry insiders view this as a critical measure to support investment certainty for new projects in the U.S.

OPIS, a Dow Jones company, provides energy prices, news, data, and analysis on gasoline, diesel, jet fuel, LPG/NGL, coal, metals, and chemicals, as well as renewable fuels and environmental commodities. It acquired pricing data assets from Singapore Solar Exchange in 2022 and now publishes the OPIS APAC Solar Weekly Report.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.