From pv magazine Germany

The downward trend in module prices across the board could not be stopped this month, but it is clearly losing momentum. Manufacturers and dealers of solar modules are still reducing their prices, but only in small steps, and seek to slowly approach the price level accepted by the market. For a long time now, nothing has been earned from products at this price level.

In China too, it’s all about minimizing damage, because unsold stocks generate avoidable costs and the risk of progressive depreciation is always present. In order not to have to pay extra for transport costs, export quantities to Europe have been drastically reduced by Asian producers in recent weeks.

Interestingly, module prices on continents other than Europe and Asia are not as affected by the price decline. The price gap is sometimes drastically different – in the United States, it is up to 100% compared to the European prices for modules with comparatively low efficiency, which means with monocrystalline PERC cells.

However, products produced in China cannot easily be redirected to America because there are strict import restrictions there. This keeps prices there high and market volume low. We will be curious to see whether the US Inflation Reduction Act (IRA) really has the desired and needed impact on local PV production capacity. At least with the currently very high purchase and installation costs in the United States, it is rather unlikely.

Transferring this model to other markets is risky, although some non-Chinese manufacturers are already celebrating and shifting their sales focus and scope of operations to the United States. An industry cannot be kept alive permanently through subsidies, we should all have learned that by now.

Chinese photovoltaic manufacturers cannot endure a sustained period of low prices for long and are already trying to stabilize prices again through artificial shortages. If demand picks up again towards the end of the year due to the current price situation, the downward trend could soon be stopped. There is hardly a market participant who is happy with the current situation.

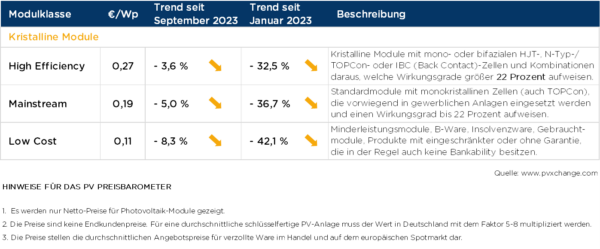

Overview of the price points differentiated by technology in October 2023, including the changes compared to the previous month (as of Oct. 15):

About the author: Martin Schachinger studied electrical engineering and has been active in renewables for more than 20 years. In 2004, he set up pvXchange.com. The online platform allows wholesalers, installers, and service companies to purchase a range of components, including out-of-production PV modules and inverters.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.