Canada’s federal government outlined a six-year investment tax credit this week that puts a 30% tax credit in place for solar, wind and energy storage projects deployed through March 2034.

The Clean Technology ITC was included as part of the Canadian government’s March 28, 2023 Budget Day fiscal priorities, with the Honourable Chrystia Freeland, Deputy Prime Minister and Finance Minister releasing the government’s 2023 federal budget titled, “A Made-In-Canada Plan.”

The Canadian government is prioritizing a clean energy economy as one of three main pillars of its multi-year budget. The federal government has a goal of making its electric grid net zero by 2035, spurring $20.9 billion in tax incentives for clean energy projects over the next six years.

Mirroring the U.S. Inflation Reduction Act as a backdrop, Canada’s Budget 2023 includes two new ITCs targeting clean energy and technology manufacturing. In the government’s remarks this week, it said the new plan allows Canada to remain competitive alongside its southern neighbor.

Clean Technology ITC

In the government’s 2022 Fall Economic Statement, it proposed a 30% refundable Clean Technologies ITC, available to eligible properties that are acquired or become available for use on or after March 28, 2023. In Budget 2023, the government expanded this ITC to apply to geothermal energy projects, in addition to solar, wind and energy storage. The term of the ITC was also extended from phasing out in 2032, as was intended under the 2022 proposal, and will remain at 30% through December 2033, stepping down to 15% in 2034 before phasing out altogether after 2034.

Clean Electricity ITC

A new incentive that the Canadian government is providing is a refundable 15% investment tax credit on the capital costs made by non-taxable entities. These include indigenous or tribal communities, municipal utilities and Crown-corporations that make investments in renewable energy, energy storage, interprovincial power transmission and other clean energy infrastructure projects.

The ITC also applies to new hydroelectric, wave/tidal projects, nuclear (including small modular reactors), and abated natural gas-fired generation.

Clean Hydrogen ITC

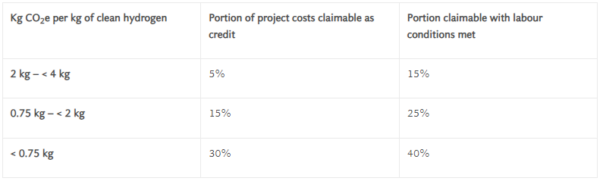

The Clean Hydrogen ITC was announced as part of the government’s 2022 proposals. New details of the basic design elements of the hydrogen ITC include a volumetric ITC credit based on carbon intensity of the project, measured by kilograms of carbon emissions produced per kilogram of hydrogen, and meeting prescribed labor conditions.

As detailed in the above chart, green hydrogen produced using the least carbon emissions and produced with claimable trained labor can see an ITC of up to 40%, while grey or blue hydrogen as its called using lesser carbon recovery can see a 5% to 25% ITC, depending on labor conditions.

Clean Manufacturing ITC

The government lined up a 30% refundable tax credit incentive for investment in machinery and equipment used to manufacture clean energy project components and extract relevant critical minerals sourced across Canada. This tax credit is available for the manufacturing of renewable energy and energy storage equipment, and the recycling of critical minerals used in EV and energy storage batteries.

Recapitalization of SREPs

Under the Budget 2023, Canada’s government pledged $30 billion in recapped investment to the Smart Renewables and Electrification Pathways (SREPs) program, a program that supports regional priorities and indigenous-led projects.

Prevailing Wage and Apprenticeships

Similar to the U.S. IRA, the Fall 2022 proposal indicated Canada’s intention to include prevailing wage and apprenticeship requirements for the proposed Clean Technology and Clean Hydrogen Investment Tax Credits. Budget 2023 proposes a wage and apprenticeship target for labor related to renewable energy, green hydrogen, carbon capture technology, and excluding zero-emission vehicles or low-carbon heat equipment. The labor requirements apply to work performed beginning on October 1, 2023.

With respect to the wage component, business owners must ensure all covered workers are paid in an amount at least equal to the relevant wage plus the value of standard benefits and pension contributions as would be provided in an “eligible collective agreement.” In provinces other than Québec, the collective agreement is generally comparable for the relevant industry and type of work performed which aligns with the worker’s duties and location. In Québec, the eligible collective agreements are those negotiated under relevant provincial law.

With respect to the apprenticeship component, 10% of total workforce hours in the relevant tax year by covered workers doing work on subsidized project elements must be done by registered apprentices.

The labor requirements apply to those workers engaged directly by the project owner or through contractors and subcontractors on project development or infrastructure projects. Labor requirements do not apply to administrative, clerical, supervisory or executives at such firms.

Canada’s Budget 2023 includes $20 billion in support of clean energy project investments, including at least $10 billion through the Clean Power priority area and at least $10 billion through the Green Infrastructure priority area as constituted by the Canadian Infrastructure Bank.

Toronto-based Westbridge Renewable Energy, a utility-scale solar developer, issued a statement applauding the Budget 2023 initiatives:

“Access to low-cost, clean energy is one of the most critical factors in helping Canada reduce carbon emissions, transition to a green economy, and foster economic growth. With Canada’s power usage expected to double by 2050, it is imperative to invest in clean technology that will help us meet that demand in a sustainable way,” said Stefano Romanin, chief executive officer of Westbridge.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.