The U.S. Internal Revenue Service (IRS) has released guidance on the Low-Income Communities Bonus Credit Program. The program provides an incentive that potentially increases the investment tax credit from 30% up to 40% for up to 900 MWdc of solar and wind, and 50% for an additional 900 MW of solar and wind power projects.

Projects in Category 1 and 2 qualify for a 10% increase to the Investment Tax Credit, while those in Category 3 and 4 qualify for a 20% increase.

Category 3 and 4 applications will be accepted first, sometime in the fall of 2023. The exact date will be announced via a website, which has not yet been developed. After 60 days, the IRS will switch to applications for Category 1 and 2.

If the program has more capacity applications than it has available capacity, the selection will be made via a lottery process. Projects are not allowed to be placed in service prior to being approved for the incentive.

There is a maximum individual project capacity of five megawatts (ac). The facilities must be placed in service within four years of receiving their award letters.

The program in the guidance is available throughout 2023 and 2024, and any excess capacity from 2024 may be carried forward and applied in 2025.

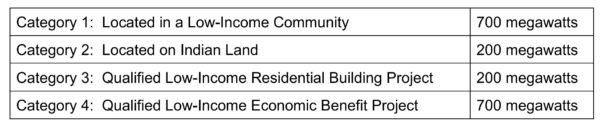

The document defines the four categories of project types:

Category 1 projects must either be located in areas with a 20% or higher poverty rate, or where the median family income is 80% of either the statewide or metropolitan area’s median family income. Category 2 projects must be located on federally designated Native American land. Category 3 projects must be installed on an affordable housing building, and the electricity must be shared equitably among the occupants of that building. The final grouping, Category 4, requires at least 50% of the financial benefits of a facility’s electricity go to “households with income of less than 200% of the poverty line … or making less than 80% of area median gross income”.

If a Category 1 or 2 project also qualifies as Category 3 or 4, then it will be considered a Category 3 or 4 facility, and will therefore be eligible for the 50% tax credit.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

What if a town is wdwrph@an IRS designated “Opporotunity Zone”? Does this mean automatice inclusion in #3 or 4? Thank you.