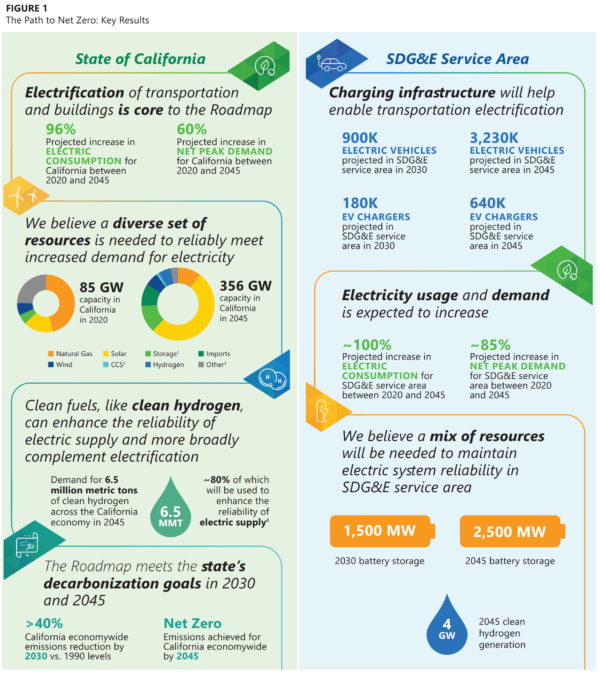

California utility San Diego Gas & Electricity (SDG&E) has released new projections for meeting California’s decarbonization goals. The study, The Path to Net Zero: A Decarbonization Roadmap for California, predicts that in order to reach the mandated carbon neutrality by 2045, the state will need to quadruple its electricity generating capacity from 85 GW to 365 GW, add 40 GW of energy storage, and integrate 20 GW of green hydrogen – while also adding 4 GW of fossil gas with carbon capture and sequestration technology.

The utility said that they believe a mix of resources will be needed to “maintain electricity system reliability in the SDG&E service area” as total consumption increases by an estimated 100%, and peak demand grows by 85%.

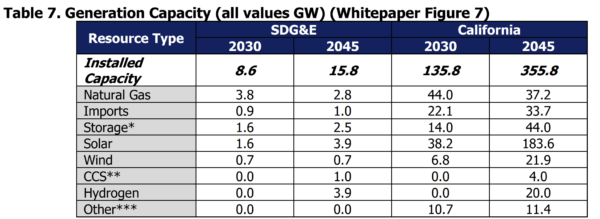

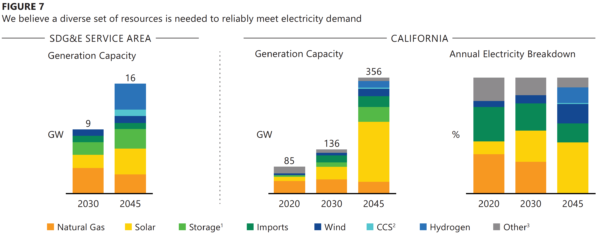

Overall generation capacities for the whole of California are projected to be 356 GW in 2045, up from 85 GW in 2020, and 136 in 2030. The SD&G service area is projected to almost double its capacity from 9 GW to 16 GW. In total, wind and solar power are projected to comprise 58% of instate generation capacity, totalling 205 GW. Utility scale solar specifically is projected to grow to 183.6 GWac, from 38.2 GWac in 2030 — and as of the end of 2020 — 12.3 GWac.

By 2045, 44% of electricity is projected to come from solar, 16% from wind, 14% from hydrogen, and 17% from imports.

The San Diego GAS & Electric company sees their fossil gas capacity falling to 3.8 GW in 2030, and 2.8 GW by 2045, while California’s fossil capacity will decrease from 44 to 37 GW. There is also the suggestion that 4 GW gas coupled with a carbon capture technology will be able to assist with the extraction of 68 million metric tons of GHGS.

However, none of the gas capacity is to be used for electricity generation as — of course — electricity is required by law to be 100% fossil free by 2045.

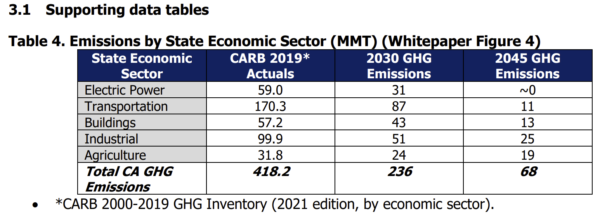

The study does see serious challenges outside of the electricity industry. Of the 68 million metric tons (MMT) of GHGs generated by the state, 25 MMT will come from the industrial sector, 19 from agriculture, 13 from buildings, and 11 from transportation.

The utility also explores the financial viability and societal equity of this transition. It is estimated that, in general, this transition will actually save money in the long term. The volume of capital needed to invest will be a “relatively small percentage of the state’s GDP.”

However, the transition might end up creating a wider gulf between haves and have nots.

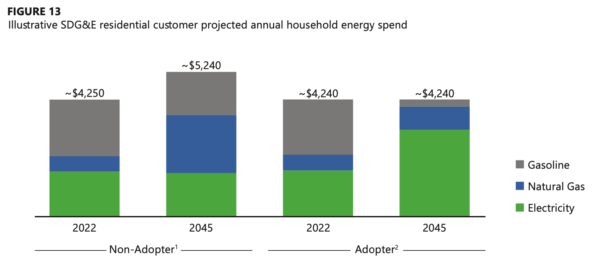

The study includes an analysis of “Adopters” of electrification – and that they are, by necessity, higher-income than “Non-Adopters”. In the long game, higher-income consumers who can afford electrification technologies (cars, heat pumps, and induction stoves for example) will eventually save more money on household energy costs, which will potentially compound existing inequities.

On average, it’s projected that households with relatively equal energy consumption bills in 2022 will see no bill growth through the next two decades. However, “Non-Adopters” will need to find 23% more income to spend on energy. This is driven by a shift from almost a third of energy coming from gasoline and fossil gas, to “Adopters”, who will get 80% of their energy from electricity.

In its own territory, SDG&E notes the transition is underway. The utility has built 3,200 EV chargers and are planning to construct larger charging networks for medium and heavy-duty vehicles like trucks and buses. They are on track to double their owned energy storage capacity to 145 MW by the end of 2022, and have another 284 MW under contract.

The researchers conclude that “in order to ensure an affordable and equitable outcome, policymakers, regulators, and SDG&E must consider how changes across the economy will affect different households, especially those of average- and lower-income customers.”

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.