Low- and middle-income homeowners (LMI) in Connecticut have had the opportunity since 2015 to sign up for no-upfront-cost solar leases, with no credit requirement.

Now, the Department of Energy’s Berkeley Labs has completed a case study on the program’s effectiveness. It found an increased rate of payment delinquencies, but noted that repayment rates were reasonable, and that the program achieved success in reaching a wider LMI customer base than typical solar lease programs.

The program is backed by Connecticut Green Bank (CBG) and PosiGen, and provides homeowners with a 20-year term with no downpayment, and no price escalator. Single-family homeowners are provided with a first-year savings guarantee, in case the PV system does not deliver the anticipated level of production.

Additionally, home energy efficiency measures were offered at a flat rate of $10 per month, covering upgrades such as insulation, advanced air sealing, and duct sealing. This began as an opt-in service, but now is included in all CBG/PosiGen LMI leases.

Findings

The Berkeley Labs report found that a majority of participants (58%) lived in census tracts having a median income of less than 80% of the area median income. By contrast, around 9% of other conventional CBG lease and loan programs lived in similar census tracts. Furthermore, 56% of CBG/PosiGen customers were reported as having “non-prime” credit scores of less than 670, compared to 2% in other programs.

Overall, the study found that payment delinquency and annualized losses were higher in the PosiGen program than for other CBG programs. It said that credit score, not income, was the prime driver. All told, 2.3% of PosiGen participants were delinquent in payments, vs. 1.4% of conventional CBG lease and loan customers. Annualized losses for PosiGen amounted to 0.9%, vs. 0.1% for other programs.

Overall, the study found that payment delinquency and annualized losses were higher in the PosiGen program than for other CBG programs. It said that credit score, not income, was the prime driver. All told, 2.3% of PosiGen participants were delinquent in payments, vs. 1.4% of conventional CBG lease and loan customers. Annualized losses for PosiGen amounted to 0.9%, vs. 0.1% for other programs.

The study found also that 44% of PosiGen participants would not qualify for standard loan or lease terms, a clear indicator of the program reaching a new pool for solar customers.

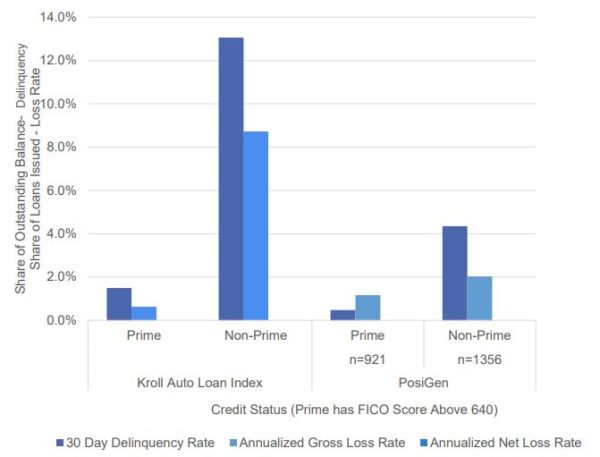

The report said that PosiGen’s program performed well when compared to benchmarks of other sub-prime loan providers. For example, the Kroll Auto Loan Index reported that customers with FICO scores below 640 have annualized gross loss rates of over 8%, and 30-day delinquencies of nearly 14%.

Program structure

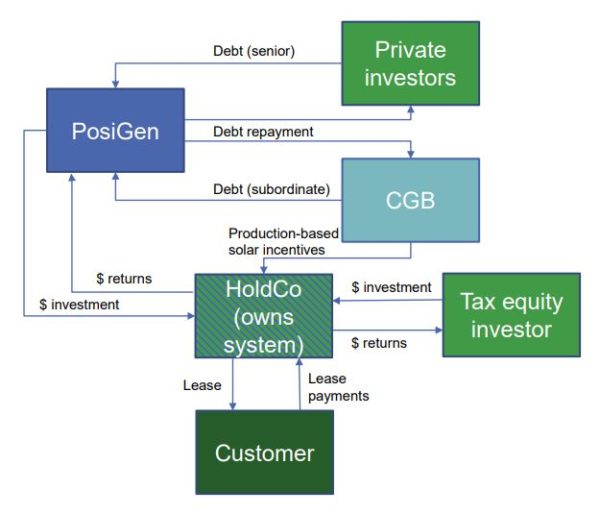

PosiGen is a private company that operates and manages solar leases. It serves as the managing member of a holding company (HoldCo) that owns the systems. Tax equity investors also own shares in the HoldCo in order to monetize the tax benefits.

CBG extends below-market-rate debt to PosiGen and pays production-based incentives (PBI) to the HoldCo. PBI is higher for LMI customers; it is paid $0.081 per kWh, according to the Berkeley Labs report.

Private investors also extend debt to PosiGen and subordination of CBG’s debt attracts these investors.

Private investors also extend debt to PosiGen and subordination of CBG’s debt attracts these investors.

HoldCo then pays back revenues to PosiGen and tax equity investors from customer lease payments and incentives. PosiGen is the primary risk-bearer in terms of customer non-payment. CBG is not affected unless PosiGen is unable to service the CBG debt.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.