Sunrun continues to carry the torch of third-party solar, as not only the largest third-party solar company but the largest residential solar company overall. The 107 MW that the company deployed is nearly double that of its nearest competitor, Vivint (65 MW), and a 7% year-over-year increase.

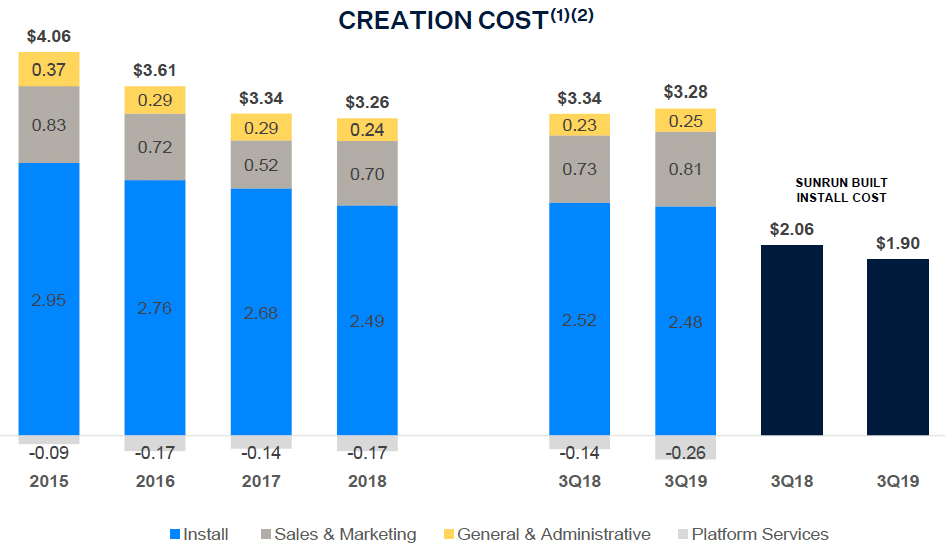

This was at the low end of the company’s guidance, and Sunrun referenced labor shortages in installation and its sales force on the company’s results call. But these are likely short-term issues, and there are deeper causes for concern about the company’s growth path. Like Vivint, Sunrun is seeing increasingly higher sales and marketing costs, which rose slightly to $0.81 per watt this quarter.

This is 10% higher than a year ago, and these costs have been rising all year. Thanks mostly to the continued decline in installation costs and a drop in general and administrative costs, the company is able to claim a slightly lower “creation cost”, but as in previous quarters this also includes around a quarter per watt in platform services revenue.

Sunrun attributes this quarter’s sales and market costs to a higher mix of direct business, but did not comment on the larger trend that the third-party solar industry writ large is facing.

Along with this, the company’s profitability appears to be flagging. Revenues rose only 5% year-over-year to $215 million, despite the aforementioned larger share of direct sales. Operating income was negative, as it consistently is for third-party solar providers, with a $60 million loss. Overall, the company’s net loss was $142 million for the quarter.

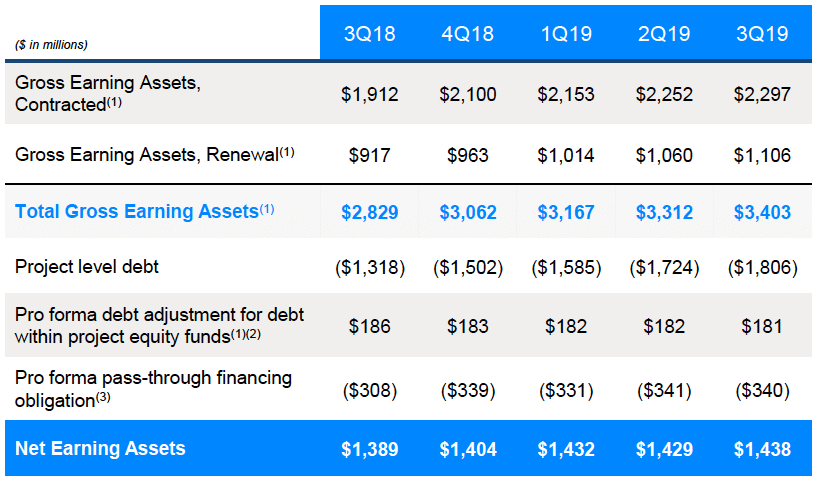

Like a squirrel preparing for winter, Sunrun is still accumulating value in its assets. However, this rose only $9 million this quarter to $1.438 billion. This metric has grown only 3.5% from the third quarter of 2018, suggesting that the value creation in its pool of assets – the main thing that a third-party solar company does – is slowing.

Overall, it is notable that while Sunrun’s quarterly installs continue to grow at a higher rate than the overall market, neither revenues or retained value is matching this rate.

That being said, the company is certainly not in any near-term danger. The first thing that a third-party solar company must do is to amass enough cash to keep deploying, and Sunrun notes that it has debt and tax equity lined up through Q4 of next year, as well as increasing its cash position by $69 million over the last year to a $373 million.

Hope for the future

Sunrun also has several factors pulling in its favor. First off, the company notes that it expects to “safe harbor” around 500 MW of PV systems under the 30% federal Investment Tax Credit (ITC) by the end of the year. And Q4 installs are expected to be a nice bump to 115-118 MW, labor shortage or no.

Another factor working in its favor is the rising demand for pairing solar and storage, and CEO Lynn Jurich wasted no time on the company’s results call noting the demand for its Brightbox system that has risen in the wake of utilities proactively shutting off power to fire-prone regions of California. Sunrun is currently reporting very high attachment rates of solar + storage in the state, which is still by far the biggest residential market.

Sunrun is clearly looking towards Brightbox, and the sale of not only this solution to homeowners but also the providing of grid services as its future. While it struggles to eke additional value out of solar under a situation of rising sales costs, these new revenues may be the future.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

This is a precise replay of SolarCity’s fall. ONE-ON-ONE SALES DOES NOT SCALE. Hopefully Tesla can pick them up for around $1.2B fall 2021.