Wood Mackenzie and the American Wind Energy Association (AWEA) today released a new report, Analysis of Commercial and Industrial Wind Energy Demand in the United States, outlining the impending corporate renewable procurement boom we are facing and how wind and solar energy fit into that boom.

The report starts off by introducing that in 2018, corporations signed more than 6 GW of power purchase agreements (PPAs), more than ever before, and provided an estimate that up to 85 GW of renewable energy demand exists through 2030 within the largest U.S. companies.

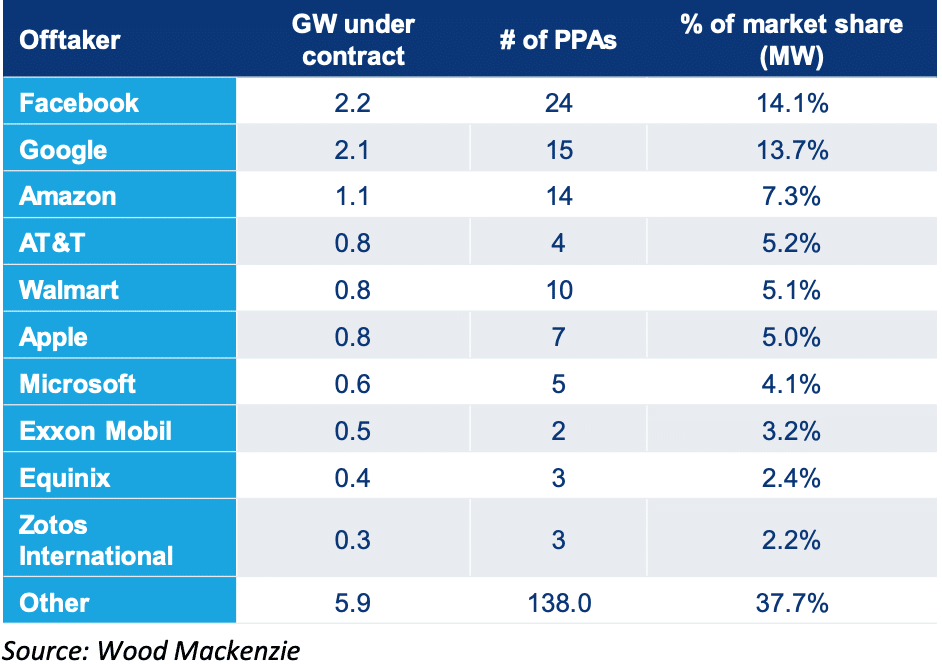

Surprise, surprise, the same companies we saw as top dogs in last month’s 2018 Solar Means Business Report, are tops all time in terms of renewable procurement. The only exception here is Target, as the company’s 229 MW come from a vast portfolio of 464 installations, mostly on the rooftops of retail stores. Since this report just tracks PPAs, Target is sitting it out.

With the capacity of renewable generation by corporations rising exponentially every year and expected to continue to do so, with the exception of an expected two-year dip when the ITC runs out, the question of why corporations are moving towards renewables becomes increasingly important. To answer that question, AWEA and WoodMac identified four key factors that accelerate adoption: branding, investor pressure, peer pressure, and the utilization of CSR to mitigate future business risks.

Those first three factors are fairly self-explanatory. The opinion that humans are contributing to irreversible and damaging climate change is a popular one that grows in popularity by the day. As more people accept it, so too will more companies, as, spoiler alert, companies are comprised of people. So between pressure from customers, competitors and investors, as well as a held belief that climate change is occurring, more companies will look to tackle this threat.

The last factor ties into this point, but not directly. What that point means is that the reasoning can be twofold. The first is that businesses feel a responsibility to stop contributing to the destruction of Earth and instead look for ways to mitigate harm or heal the planet. Because of this, not only does the company gain positive approval from outsiders, but the company is also combating climate change, the effects of which could substantially impact the operation of said company.

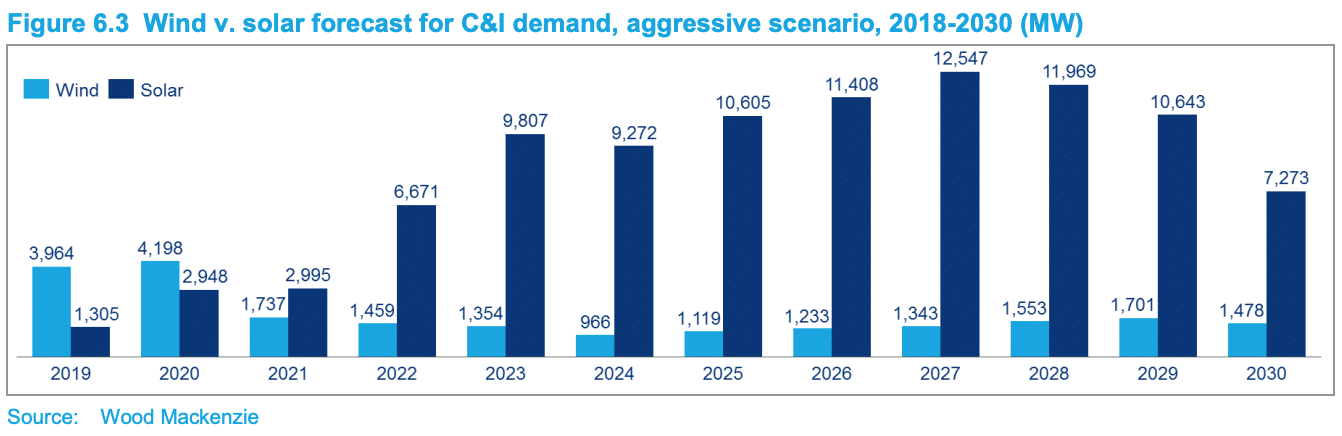

However, the most interesting content in the report came at the very end. Starting in 2021, the most aggressive projections WoodMac has anticipate corporate adoption of solar to overtake that of wind, and as far as the report projects (2030), it never looks back. In fact, forget looking back, the gap between solar and wind adoption is set to grow dramatically year over year, reaching its peak in 2027, when WoodMackenzie predicts companies will contract for over 12.5 GW of solar energy, compared to only 1.3 GW of wind. In the first year of the takeover, 2021, corporations are anticipated to adopt nearly 3 GW of solar, compared to 1.7 GW of solar.

In fact, wind’s drop off is a dramatic one, overshadowed by the frenzied climb of solar. It’s an ungodly number to think about now, but the report’s most aggressive projections predict total corporate solar adoption through 2030 to come in at 97 GW. This is compared to 22 GW over the same period for wind. Through 2030 wind adoption is never expected to reach half of the 4.2 GW mark anticipated for 2020, with a low of 966 MW predicted for 2024. It should also be noted the significant decrease predicted for solar every year following that 12.5 GW 2027 peak. Again, it should be clarified that these are not the expectation, but rather aggressive projections.

It’s not that wind as a resource is doomed by any means, and it is not this writer’s intent to put-down wind as a generation source. Wind, like solar, just cant do it all on its own. As the report puts it:

Absent of a step change in turbine performance or cost reductions, it is increasingly obvious that for wind to compete amidst ever increasing renewables penetration, a longterm energy storage solution must be developed to cope with wind’s weekly and seasonal boom/bust cycle.

In short, solar’s biggest advantage over wind is that it’s more predictable and easier to forecast generation figures. However, as is the case with solar as well, wind projects will be best served to become wind + storage projects. For these intermittent sources, the ability to store generation will be just as valuable as the sun and wind moving into the next decade and beyond.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.