For those waiting for the moment when we could see a distinct impact from the Section 201 tariffs imposed by U.S. President Donald Trump, the second quarter of 2018 was it. Solar installation levels across all sectors fell to 2.3 GW-DC, a 9% fall year-over-year and a 7% decline versus the first quarter.

But if anything, the details of the latest U.S. Solar Market Insight report put out by Wood Mackenzie (formerly GTM Research) and Solar Energy Industries Association (SEIA) show the resiliency of the solar industry. The report shows a record 8.5 GW of solar being procured in the first half of 2018, which it says will lead to a distinct rebound in the second half of the year.

Trade wars and module supply

The key to all of this may be in the dynamics of trade relations between the United States and China and the complicated circumstances of PV manufacturing. Since 2012, the U.S. government has been trying to stem the tide of low-cost, heavily subsidized solar from China in a series of trade cases.

The reaction from Chinese PV makers was first to shift to using Taiwanese cells, heralding the rise of some of the world’s largest cell makers in Taiwan. Then when the United States slapped tariffs on China and Taiwan in 2014, these same companies moved manufacturing to Southeast Asia.

The global nature of the Section 201 tariffs made it impossible to continue moving factories around the world. But less than four months after these tariffs were imposed, China did a u-turn on policy support for its domestic solar industry, sending prices plummeting.

No there is nothing to say that China did this to undo the impact of the Section 201 tariffs, as there are domestic reasons why it could have chosen to reform its solar compensation programs. But whether intentional or not, the action had the same effect of making the tariffs largely moot.

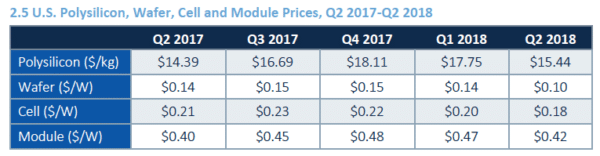

According to Wood Mackenzie, the average price of multicrystalline PV modules in the United States in the second quarter was only $0.42 per watt – the lowest it has been for a year, despite the 30% tariffs on imported modules.

However, it is likely that the U.S. market was already on the rebound by the time that Chinese prices hit. One under-appreciated aspect of policy changes like the Section 201 tariffs is that the uncertainty caused by the process can be as bad, or worse, than the actual policies.

As many developers have expressed to pv magazine, once the tariffs were set deals could go forward again, because even if they were less favorable, developers, off-takers and project financiers finally knew what the numbers were.

Sector breakdown

While only 1.2 GW of solar was installed in the utility-scale sector, there is currently a total of 4.3 GW of utility-scale projects that are under construction, along with another 20 GW where contracts are signed but construction has not yet begun. Many of these will likely try to get in under the 30% investment tax credit, which can be claimed if projects begin construction by the end of next year, even if they don’t go online until the end of 2022.

Wood Mackenzie’s “non-residential” sector did not fare as well, and the 453 MW installed is down 8% from a year ago. The saving grace of this sector was commercial solar, which saw a whopping 300 MW installed, largely in Minnesota and Massachusetts.

Meanwhile the residential sector is showing that it at least is not continuing to crash. While installations are still below 2016 levels, they were relatively flat year-over-year during the second quarter. And while most of the largest solar markets are still showing declines, installation is moving to second-tier markets as this market becomes more national and less focused on a few key states.

Outlook

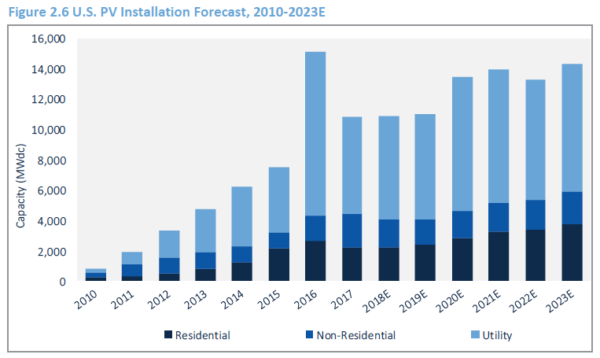

Wood Mackenzie is forecasting that even with the rebound in the second half of the year, 2018 installations will be flat versus 2017 at around 10.9 GW-DC. The company predicts another flat year in 2019, with growth resuming after 2020 as projects taking advantage of the tail end of the ITC come online.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.