The United States is in the middle of an unprecedented rush by both independent power producers and utilities to build natural gas plants and pipelines. While natural gas has largely led capacity additions throughout the first two decades of the 21st century, the U.S. Department of Energy’s Energy Information Administration (EIA) forecasts that a stunning 21 GW of natural gas-fired power plants will come online in 2018, more than any year in at least a decade.

Along with this, EIA is projecting a record buildout of gas pipelines in the Northeastern United States in 2018, as a Trump appointee-led Federal Energy Regulatory Commission (FERC) eases the process to build new pipelines.

This is just the beginning. According to a new report by Rocky Mountain Institute (RMI), 110 GW of gas projects have been announced for construction through 2025. These plants and associated pipelines to feed them will come with a $112 billion price tag.

However, this “rush to gas” comes at the same time that wind, solar and battery storage costs have fallen enough to make clean energy a viable alternative. This is not speculation, as combinations of renewable energy, energy efficiency, demand response and grid infrastructure are already replacing existing gas and other fossil fuel plants in California.

Stranded assets

RMI’s The Economics of Clean Energy Portfolios notes that, in many cases, these gas plants are being built to replace the older generation, including aging coal and nuclear power plants. Over half the U.S. thermal generation fleet is more than 30 years old and expected to reach retirement by 2030, and RMI estimates that it would require $500 billion to replace all of these plants with gas generation. This would lock in a combined $1 trillion in asset and fuel costs.

This would also result in 5 billion tons of CO2 emissions through 2030, with that number increasing to 16 billion tons through 2050. With these emissions comes the release of methane (CH4), a far more potent greenhouse gas over 20 and 100-year timeframes.

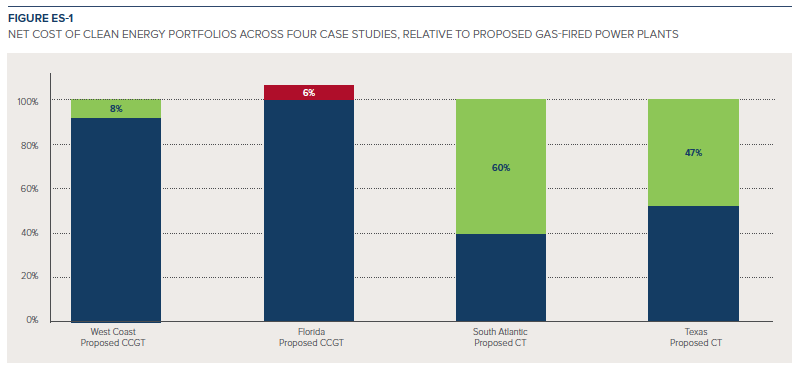

None of this is necessary. RMI conducted case studies of four natural gas-fired power plants currently proposed for construction across the nation and found that in three of four cases, the optimized portfolios of renewable energy and other non-emitting resources could replace the gas plants at a lower cost. In the fourth scenario, RMI found that the clean energy portfolio would cost roughly 6% more.

These are at current costs for clean energy resources, and do not include a price on carbon. RMI found that when factoring in a modest $7.50 per ton cost of CO2 and expected price declines for distributed solar, clean energy is the cheaper alternative in all cases.

These clean energy options showed generally superior economics versus both combined cycle gas plants and combustion turbines, which have different use cases. Combustion turbines are typically used as “peaker” plants, running seldom and in times of high demand, wheres combined cycle plants tend to run more often as “mid-merit” plants.

The clean energy portfolios modeled by RMI have the ability to provide not just energy, but also the ancillary services required by the grid.

RMI warns that as such, these gas projects risk becoming stranded assets, with consequences for everyone involved. “The consequences of continuing a business-as-usual approach—building new gas generation when clean energy technologies are increasingly winning the day—promises to negatively impact customers, investors, and the environment through higher energy costs, the risk of stranded assets and greater carbon and air emissions,” warns Mark Dyson, a principal at RMI and author of the report.

Investors in more danger than electricity customers

Of the $112 billion in gas plants currently proposed or under construction, 17% are under the jurisdiction of monopoly utilities, and are being enabled by state regulators. This means that the customers of these utilities are ultimately on the line for these unnecessary costs.

In many cases, such as Michigan Public Service Commission’s (MPSC) recent decision to allow DTE Energy to build a new gas plant, regulators are beginning to express misgivings about their own failure to adequately consider alternatives. Even so, neither this nor strong public objection stopped MPSC from approving the project.

However, the $19 billion in locked-in costs faced by consumers across the nation is not the biggest bill. Independent power producers are planning to invest $93 billion in gas infrastructure for competitive wholesale power markets, leaving these companies and their shareholders with any stranded assets.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.