The U.S. residential solar market has changed dramatically in the past few years. With both policy headwinds, market challenges and two of the three largest residential installers undergoing dramatic internal changes, the U.S. residential solar market fell significantly in 2017 – its first year of decline in recent memory.

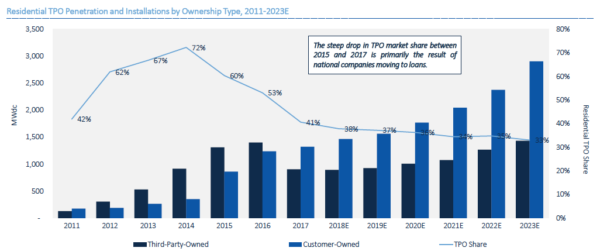

As the market contracted, the share of residential solar deployed under leases and power purchase agreements (PPAs) has also fallen, and beginning in the fourth quarter of 2016 the market share of customer-owned solar surpassed that of third-party solar. The third-party portion has declined since, with a new report by GTM Research finding that solar deployed under leases and PPAs fell to less than 40% of residential deployment by the end of 2017.

As this was happening, SolarCity under new owner Tesla was withdrawing form the third-party market, as has Vivint Solar to a lesser degree, while both companies significantly scaled back installations overall.

This presents something of a chicken-and-egg question. Did the share of third-party solar decline due to the actions of Tesla and Vivint? Or did both companies respond to changes in the market?

Either way, the landscape has changed, with a new leader emerging: Sunrun. The company became the nation’s largest residential solar installer by the end of 2017, and has also captured the biggest share of the third-party solar space.

According to GTM Research, in the last quarter of 2017 Sunrun captured a full 32% of all third-party solar sales, compared to Tesla’s 23%, and Vivint’s 16%. However, Sunrun is increasingly dominating a space which is not showing as great of potential as customer-owned solar. GTM Research predicts flat growth in third-party solar in 2018 and 2019, and modest growth for the following four years.

Mosaic leads solar loans, finance overall

As the third-party space stagnates, GTM Research is predicting much more rapid growth in customer-owned solar. This is largely credited to the increasing availability of a wider range of loan products.

These loans are being provided by a combination of traditional lenders and new companies which have emerged to provide solar-specific finance products. Solar loan provider Mosaic, which got its start in “crowd-funding” solar, has since become the largest financier of residential solar in the United States.

GTM Research attributes this in part to the company’s supply of solar loans to Tesla, but the company is also working with more than 150 other solar installers. Sunlight Financial has also grown significantly in 2017, which GTM Research also attributes to its relationship with a few large installers.

And this busy space is starting to heat up. “This intense competition has led to uber-competitive rates and therefore compressed margins, leaving questions about the financial health and long-term viability of many of these loan providers,” notes GTM Research.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.