It’s no secret that North Carolina has become one of the nation’s largest solar markets, driven by favorable implementation of federal laws requiring renewable energy procurement, a state tax credit, and one of the first renewable energy mandates in the South.

However, a new report by Southern Alliance Clean Energy (SACE) shows that it is not only North Carolina that is an important market for solar growth in the southeastern United States. Neighboring South Carolina is also on a path for ambitious solar deployment, with Florida and Georgia also emerging as significant state markets

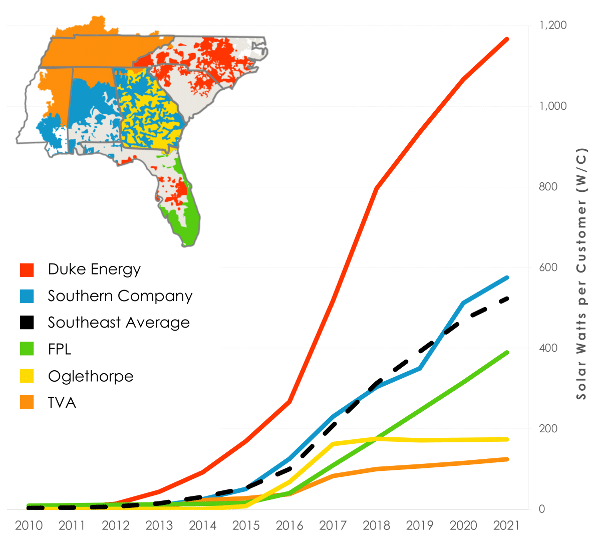

Solar in the Southeast is envisioned by SACE as an annual report series, and the first report measures progress in the region by both utility and service area. The report includes the important metric of watts per customer, which can show the relative progress of smaller utilities with fewer customers and less populous states versus their larger neighbors.

In measuring progress by utility, Duke Energy Progress, whose service area covers parts of North and South Carolina, has by far the largest capacity of solar on a per-customer basis among large utilities. Progress clocks in at 1,117 watts per customer as of 2017, with second place Duke Energy Carolinas at a mere 474 watts per customer.

In measuring progress by utility, Duke Energy Progress, whose service area covers parts of North and South Carolina, has by far the largest capacity of solar on a per-customer basis among large utilities. Progress clocks in at 1,117 watts per customer as of 2017, with second place Duke Energy Carolinas at a mere 474 watts per customer.

The combination of state and utility rankings is telling; however it is important to note that in the Southeast utilities have only recently emerged as willing partners to the energy transition. North Carolina’s policies to support the solar industry were hardly driven by utilities. Most importantly, the developer-friendly implementation of the Public Utilities Regulatory Policies Act of 1978 (PURPA) that has been a main driver of that state’s market was actively resisted by Duke for years and has now been modified.

The same can be said of Georgia, which has the second-largest installed capacity to date. Georgia Power resisted solar in its service area for years, but after being pushed into adopting solar by regulators, the utility now has the third-highest watts of solar per customer among large utilities in the region at 364 MW.

In all of these states it is important to note that deployment to date has been driven by large-scale projects, with much lower levels of behind-the-meter, customer-owned solar.

South Carolina, Florida to take off

Looking forward, the report expects substantial growth in North Carolina, and also for South Carolina’s solar market to move rapidly. In South Carolina, SACE credits legislation passed in 2014 that covers net metering, utility procurement and third-party leasing. While South Carolina was already in second place at 318 watts of solar per utility customer in 2017, the report expects this to grow 170% to 856 watts per customer by 2021.

The report is also expecting Georgia’s solar market to nearly double to 476 watts/customer, and Florida to show more than four-fold growth to 425 watts per customer. In both states, much of this is driven by large-scale solar projects that have already been announced.

In Georgia this has taken the form of contracts through Georgia Power’s Renewable Energy Development Initiative. This includes the largest solar project in the South, which First Solar will be building. In Florida multiple utilities including Duke Energy Florida, Florida Power and Light, Tampa Electric, Jacksonville’s municipal utility and even the semi-public utility that provides power to Disneyland have all announced large solar projects over the last year.

In many cases smaller utilities are expected to move even faster. The report finds several municipal utilities in North Carolina to reach more than 3,000 watts of solar per customer in 2021. But the top spot in the region goes to the municipal utility in the city of Orangeburg, South Carolina, which already has nearly 3,000 watts of solar per customer and is expecting to reach more than 5,400 watts of solar for each of its 24,000 customers.

In contrast to this progress, the report is critical of slower progress on both statewide policies and utility ambitions in Alabama, Mississippi and Tennessee, and specifically mentions Tennessee Valley Authority (TVA) as a utility whose commitment to renewable energy is “waning”.

But TVA is not the most regressive utility in the South as regards renewable energy. An interesting wrinkle to the report is that SACE’s definition of the “Southeast” does not extend west of Mississippi, meaning that it covers the entire Deep South except Louisiana, and furthermore does not cover Entergy’s service area in Mississippi.

If it did, it would no doubt bring down the averages, given that Entergy – the nation’s second-largest operator of nuclear power plants – has been one of the most resistant power companies in the United States to renewable energy and has built very little large-scale solar to date.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.