The solar industry is well known for its cycles of boom and bust, and this is reflected in capital flows into the industry. After two years of boom 2016 went bust, with a drying up of capital and depressed stock prices across the industry due to both a hangover from the expected drop-down of the investment tax credit (ITC) as well as a faulty association between oil prices and the prospects of solar.

According to the latest report on solar funding and mergers and acquisitions by Mercom Capital, 2017 showed relative recovery. The firm reports that largely on a year-end push total corporate funding rose 41% in 2017 to $12.8 billion, buoyed by a number of factors.

“Higher installation levels around the world, the lack of threat to the solar investment tax credit, lower than expected tariff recommendation by U.S. ITC, strong debt financing activity, and over a billion dollars in securitization deals helped the solar industry have a much better year in terms of financial activity compared to 2016,” explained Mercom CEO Raj Prabhu.

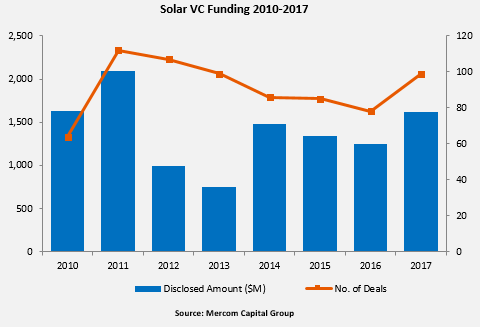

Leading the good news is an increase in venture capital (VC) funding, which rose 30% to $1.6 billion in 99 deals during 2017. Prabhu notes several large private equity deals in India, and downstream companies continued to dominate, representing 85% of the total investment.

The top venture capital/private equity investments in 2017 were BP’s $200 million investment in the UK’s Lightsource Renewable Energy, and two $200 million investments in India’s ReNew Power.

For solar technology enthusiasts, there is the good news that thin film companies also raised $104 million, however this is a fraction of what such companies raised in 2011 at the heyday of innovation in this space.

The volume of announced debt financing to solar companies also increased more than 50% in 2017 to $9.5 billion. These two metrics were matched by an increase in the valuation of solar stocks, with the Guggenheim Solar Exchange Traded Fund – which Mercom Capital does not track – rising from below $18 per share at the beginning of 2017 to around $26 on January 3.

Despite this public market financing was flat, with only $1.7 billion raised in 33 deals, and three initial public offerings raising $363 million. And Chinese solar companies may be beginning to leave Western stock exchanges, as indicated by Trina Solar going private in a $1.1 billion transaction.

Mixed results from DG financing

While large-scale project financing increased nearly 50% to $14 billion, distributed solar financing showed more of a mixed year in 2017. This may reflect the decline in the overall market volume in the United States, with the residential sector hit hard by a mixture of pull-back from large installers, policy changes and exhaustion of the first-adopter demographic.

Securitizations reached $1.3 billion, as the first year netting more than $1 billion, however the total volume of residential and commercial solar project funds fell 50% to only $2.4 billion. Prabhu notes that this fall in project fund levels is related to the pull-back from large national installers, as smaller local installers typically do not raise funds, but instead rely on loan providers or third-party financing providers.

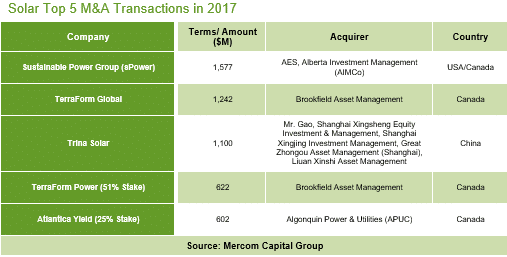

Mergers and acquisitions were also on the rise, with 72 corporate M&A transactions. As is the case with VC funding the downstream sector showed itself to be the most dynamic, representing 51 of the 72 transactions. This included AES and Alberta Asset Management’s $1.6 billion acquisition of developer sPower, and Brookfield snatching up TerraForm Global for $1.2 billion.

And while the net result was relatively positive, Mercom Capital warns that there could be severe fall-out if President Trump imposes heavy sanctions on global imports under the Section 201 case. The president is due to issue a decision on the case by January 26, and all indications point in the direction of strong trade action.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.