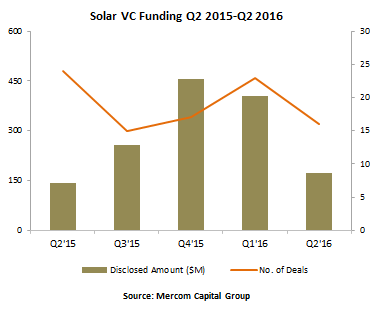

Mercom Capital’s latest report on solar funding and merger and acquisition (M&A) activity does not paint a pretty picture of the sector. The report finds that Q2 2016 venture capital funding fell by more than half while debt funding fell 43% from the previous quarter. Public market financing remained at only $179 million, more than double last quarter but less than 10% of the level achieved a year ago.

The result is a 41% collapse to only $1.7 billion in all sources of corporate funding during the quarter, the lowest level of financing in three years.

Mercom CEO Raj Prabhu notes that Q2 was a continuation of the decline seen in Q1, and that the ill fortune of the solar industry coincides with a number of factors, citing SunEdison’s bankruptcy and the collapse of yieldcos. However, the biggest factor cited by Prabhu is the ongoing decline in solar stocks, spurred not only by high-profile bankruptcies but also the ongoing collapse in oil prices and other factors.

“All of these things have made the public market valuations lower, and with lower valuations it becomes expensive to go out and raise money,” Prabhu told pv magazine. “We’re hoping that it bottoms out now, because it is as low as it can go.”

Another factor cited by Prabhu is policy uncertainty. Despite the extension of the federal Investment Tax Credit, investors have been spooked by the retroactive and very damaging changes to Nevada’s net metering policy, fearing that this may happen in another state.

Despite these concerns, one bright spot in the report was the ongoing growth in distributed solar project funds. During the quarter residential and commercial solar funds grew 36% sequentially to $1.36 billion in 11 deals, led by SolarCity, Mosaic and Sunnova Energy.

Of this $1.36 billion, $800 million went towards third-party funds and $555 million to loan funds, and Mercom notes that since 2009 residential and commercial solar funds have raised almost $20 billion.

There were also 17 solar mergers and acquisitions in the second quarter of 2016, up from 14 in the previous quarter. Eight of these involved downstream solar companies, and five involving balance of systems players. Of these, Sungevity’s plan to go public through a $357 million deal with a Massachusetts-based asset management firm is likely the most significant.

More than 2 GW of solar projects were acquired in the second quarter, down from 2.4 GW in the first. Mercom notes that project acquisition has slowed due to less activity from yieldcos, three of which are associated with bankrupt solar companies Abengoa and SunEdison.

This slowdown is set against a larger trend of growth in project acquisitions. “We will have to wait for another quarter to see if the trend continues,” notes Prabhu.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

6 comments

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.