On the eve of summer last year, not everything was rosy in the garden of EU, but few could have foreseen the tumult that was to come. Beginning with the steady drip-drip of refugees and migrants serving to destabilize formerly harmonious border relations, the past year has seen Europe haunted by the specter of a return of old divisions, traumatized by deadly terrorist attacks, and pensive over the direction of many of its leading economies.

With the U.K. due to hold a pivotal In/Out EU referendum around the time you read this, Spaniards being asked to go back to the polls to vote through the deadlock of last December’s general election, and the low approval rating for German Chancellor Angela Merkel, it has been many decades indeed since the continent had to face so much uncertainty.

But the onset of summer brings not just sunny skies, balmy evenings and billions of extra euros to the coffers of Europe’s poorer – but more popular – nations: It also brings hope of a more unified future. The European Soccer Championship, for example, is currently underway in France: a sporting spectacle that showcases the best in European solidarity, creativity and friendly rivalry. Then, come July, the U.K. could well be doubling down on its efforts to forge a better EU following an ‘In’ vote, and Spain may have a government in place able to maintain the course of its economic revival.

Which brings us on to the continent’s solar market. Perennially a snapshot of Europe’s layered nuances, PV has experienced another mixed 12 months in Europe. Rising in places, falling in others, stabilizing in corners of the continent that should, in truth, have more solar installed, and emerging in regions where the sun is something of a stranger, there is no easy way to take the pulse of PV in Europe without breaking it down, nation by nation. Which is exactly what pv magazine’s international posse of PV correspondents has done.

Germany: the sleeping green giant

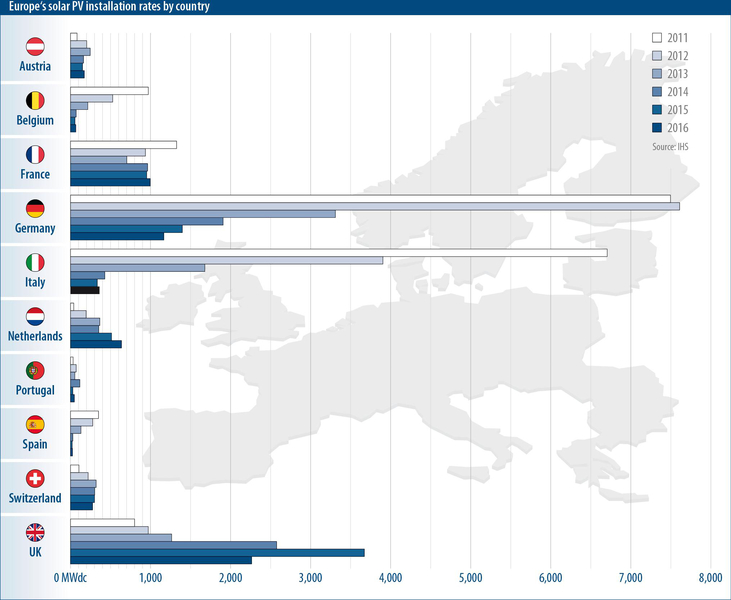

In Germany, newly installed capacity has stabilized at 1.5 GW per year, which is below the stated political goal of 2.5 GW. In the first quarter of 2016, newly installed capacity amounted to just 211.5 MW. Yet the political establishment in Germany is currently doing little to spur demand. The German government is working on a revision of the Renewable Energy Act (EEG), which will change the funding scheme for PV and wind power from a feed-in-based system to one based on a tender process. There are still major disagreements between the German federal and state governments. The plan is to pass reforms in Parliament by summer.

The current draft law stipulates that only ground-mounted or rooftop PV arrays with capacities of 1 MW and up would have to be subsidized through the tender process. All smaller systems would continue to receive incentives through FITs or a merchant basis. The German solar industry welcomes this threshold.The fear, however, is that in the course of the parliamentary process this limit will be lowered, which will not be without consequences.

Last year saw the first three pilot tenders for ground-mounted systems. In the process, the government awarded 101 contracts for PV plants with capacities totaling more than 500 MW. Another call for tenders was issued in April 2016, which ended with the awarding of contracts for a further 21 solar farms with a total of 125 MW of capacity. In this most recent round of tenders, the value of the contracts awarded turned sharply downward. In April, the lowest successful bid was just €0.069/kWh, and the average value for successful projects was €0.0741/kWh. In the first round of tenders in April 2015, the average price was still at €0.0917/kWh.

So far, all of the tender rounds have been oversubscribed. However, many of the successful projects in the calls for tender have not yet been built. By this spring, only a handful had been completed. This is having a negative impact on expansion because ground-mounted systems are no longer subsidized outside the tender process. “At present, the trend in capacity expansion is pointing toward 1 GW,” says Carsten Körnig, Chief Executive of the German Solar Industry Federation. “Whether we reach 1.5 GW this year depends largely on how many tender projects are realized.” Once a contract is awarded, successful bidders have two years to build their ground-mounted PV plants. Many investors are speculating on falling prices and will probably not be implementing their projects anytime soon.

Sandra Enkhardt

U.K.: Solar’s seed is sowed

In 2011, the U.K. installed 223 MW of solar. Last year, that figure was 3,537 MW, according to data published by the Department of Energy and Climate Change (DECC). Cumulatively, PV capacity in the U.K. stands at just over 9 GW, providing 9.1% of all renewable energy output in 2015 – an 86% increase in solar electricity generation in the space of a year, topping 7.6 TWh to boot.

Such naked data would seem to suggest a market that is surging ahead at breakneck speed. Which it was, for a while. In context, however, 2015 is likely to represent a peak for PV installations in the U.K., at least for a few years. Stymied by recent subsidy adjustments, 2016 post-April 1 – when the latest cuts to the renewable obligation certificate (ROC) were enacted – is shaping up to be comparatively moribund, installation-wise.

The U.K. will end the year with around 1.9 GW of additional PV capacity (according to Bloomberg New Energy Finance forecasts), but much of that was installed under pre-cut rush conditions in the first quarter of the year – which suggests what, exactly? The old policy framework that was incorporated by the previous coalition government of the Conservatives and Liberal Democrats was quickly abandoned once the former party took complete control last May. That the Tories are anti-renewables is no secret, but what the maturation of the U.K. solar industry has revealed is that – despite government reticence on solar power – the great British public has taken PV to its heart.

With more than 750,000 residential homes now fitted with rooftop PV arrays, Brits are fast embracing solar. The last xAdvertisementround of FIT cuts was painful for homeowners – slashed 64% from GBP 0.1247/kWh to GBP 0.0439p/kWh (for systems < 4 kW) – but the advanced warning prior to the cut’s enactment (the new rate applied on February 6 this year, and the cuts were announced in September last year) fuelled a 59% increase in FIT-based rooftop installations during that time frame. And even with the reduced FIT rates, a recent study by the Solar Trade Association (STA) found that solar still makes economic sense, delivering homeowners a 5% tax-free return on investment over 13 years, and adding an average of $3,000 to a typical property’s value.

At large scale, the early closure of the ROC scheme on April 1 (having also been reduced to 1.3 ROC a year ahead of schedule in 2015) triggered the anticipated rush of installations, with the first quarter of 2016 serenaded to the sound of email pings in pv magazine ’s inbox announcing the connection of yet another 20 MW+ array somewhere in the country.

With solar panels a common sight on rooftops in British cities, and ground-mounted farms no longer provoking the ire of the NIMBY (Not in My Backyard) set as they once did, the acceptance of PV has grown. DECC’s own survey in April found that 84% of the public is supportive of solar energy – the highest backing for any energy technology ever recorded in its Public Attitudes Tracker.

This support should not be underestimated. With the U.K. economy currently one of the strongest in Europe, and Brits eager to play their part in helping the country meet its carbon reduction obligations, solar – despite its near abandonment at top level – enjoys unprecedented support, and its increasing affordability will likely convince more home and business owners to adopt the technology.

There is, however, one major fly circling the ointment: the looming threat of Brexit. Current polls put the ‘In’ camp ahead on 55%, but the vote is uncomfortably close for many. There are some arguments that suggest a Brexit could, in the short term at least, provide a fillip for the British solar industry. Leonie Greene, head of external affairs at the STA, told pv magazine that the issue is complex because, on the one hand the minimum import price (MIP) levied by the EU on components from China is “really hurting the industry,” but the bigger picture is one of a longer-term game, she said.

David Hunt, managing partner of clean energy firm Hyperion, is worried what a Conservative government could do to the U.K.’s renewables industry with the EU “shackles” removed. “No MIP for U.K. solar would of course bring a short-term benefit, but that in itself is not a reason to be in favor of Brexit,” he said. “There are significant other considerations, not least further weakening of government policy towards renewables with the legal carbon and environmental obligations that come with EU membership.

“We have a government that has already done as much as it can to disadvantage the renewable sector, solar in particular. With the EU ‘shackles’ removed,” Hunt continued, “we would likely see a further erosion of the legislation and drivers the industry needs to thrive.” In May a report by Ernst & Young ranking countries’ renewable energy attractiveness saw the U.K. slip to its lowest-ever position of 13th , with the government’s muddled approach to the sector to blame. “A non-committal approach is putting the attractiveness of the U.K.’s renewable energy on a landslide,” wrote Ernst & Young global power & utilities corporate finance leader Ben Warren. A U.K. free from EU regulation on environmental concerns would likely slink further from the progress the country has made in supporting its solar industry. However, despite the harbingers of doom an ‘Out’ vote could elicit, Prime Minister David Cameron – committed to the EU – could well be out of office come June 24, so who is to say in which direction the country will then go?

As things stand, the U.K. is an EU member, likely (however narrowly) to vote to stay in, and perhaps likely to discover a renewed vigor for backing the EU on matters close to Britain’s heart. And if recent evidence is anything to go by, PV is part of that bracket.

Ian Clover

France: steady as she goes

Last year was a positive one for France’s clean energy landscape, with several measures favorable to solar implemented. In particular, a decree to be published in the next few weeks and approved by Industry body Conseil Superieur de l’Énergie looks set to triple the current solar PV goal by 2023 to 20.2 GW. The IEA reports that by the end of 2015, PV grew by 879 MW, bringing cumulative capacity to 6,549 MW. Including overseas territories, France reached 6.5 GW of installed PV by the end of 2015 and produced 6.7 TWh of solar energy. According to the Ministry of Energy, Ecology and Sustainable Development (MEDDE), this accounts for 1.4% of electric demand met by PV in 2015. Last March, MEDDE released 2015 solar market figures that showed, in addition to the 897 MW of solar PV installed, a further 559 MW of PV plants have signed interconnection agreements but have not yet been connected.

The policy framework has been evolving in the past few years, thanks to a decisive direction taken by the government towards clean energy. This stance was evident last year with the enactment of the Energy Transition Act for Green Growth and the United Nations on Climate Change Conference (COP21), held last December in Paris. The Energy Transition Act for Green Growth was passed by the French Parliament in August 2015, and creates a new support mechanism for renewables above 0.5 MW (starting 1 January 2017), in which energy will be sold directly on the electricity market at a premium. The multi-year energy plan (PPE), due in July, will set out the specifics.

Several PV promotion policies have also been set up in the country’s regional, departmental and municipal authorities. The regions of Alsace, Aquitaine, Guadeloupe, Languedoc-Roussillon, Pays de la Loire, and Poitou-Charentes have issued calls for proposals for PV self-consumption projects. At a local level, Paris is a good example for municipalities implementing eco-district projects: The houses of the new headquarters of the French Ministry of Defense feature an 820 kW array and a low energy building in the 15th arrondissement in Paris was inaugurated in November.

A national policy of FITs is in place in France. The tariffs for purchase of electricity from PV connected to the grid have been lowered in the first quarter of 2016, and the French Commission for Energy Regulation (CRE) published in February the coefficients to calculate the reduction of the FIT rates for rooftop PV systems with a power of up to 100 kW.

Alternatively, PV systems above 100 kW can apply to calls for tenders. They are guaranteed over a period of 20 years and paid for by electricity consumers. Data about the tenders can be found in the 2015 IEA report “Snapshot of Global PV Markets.” IEA explains that the CRE launched two calls for tenders. The first was for rooftop systems (100 kW to 250 kW) for a total volume of 240 MW, totaling 80 MW of cumulative capacity.

The list of the 349 winning projects was published in March by the Ministry of Energy, Ecology and Sustainable Development. The second is for the installation of 50 MW of PV plants (> 100 kW) with storage in non-interconnected territories. The results of the CRE3 call for tenders were released at the end of the year, with a total power of 1,100 MW. Additionally, the ministry published a calendar of new calls for tenders for a total of 4,350 MW between 2016 and 2019.

Anna Favero

Dutch display courage

While promising, considerable uncertainties are undermining confidence in the Dutch PV market. A lack of success in recent SDE+ large-scale renewable tender rounds compounded by a looming review of the residential net metering program has left the sector laboring under an atmosphere of uncertainty.

“In the last few years, there has been incredible growth due to the residential market,” explains Cees van de Werken, the Founder of distributor ProfiNRG. “Today, however, there is no visibility as to what the future may be. In 2016 it is crucial that new SDE+ projects get awarded because if there are no new projects that is a huge risk for the market.” Large-scale renewables are incentivized in the Netherlands under its biannually awarded SDE+ subsidy program (Stimulering Duurzame Energieproductie/Encouraging Sustainable Energy Production). The Dutch government allocates €8 billion annually for the program, but the tender process is technology agnostic, with 2015 and the first tranche of 2016 allocating only a small number of successful bids to PV. Wind and biomass/biofuel were awarded the lion’s share, delivering an average kWh cost under the SDE+ program of around €0.12/kWh, a result the Dutch Economic Affairs Minister Henk Kamp welcomed. In such a low tender price environment and with the country’s relatively meager irradiation, PV struggles to compete on cost.

“Last month it was reported that 1,200 to 1,300 solar projects applied for the [autumn tranche of] SDE+ but the impression is that no solar projects will be awarded because of the payback time, which needs an SDE+ of €0.128 over 10 years,” says ProfiNRG’s de Werken. He notes that despite this, some developers will still bid below €0.11/kWh in the hope that falling component prices will allow projects to go ahead.

Dutch PV developers have displayed a degree of inventiveness in pursuing projects, with the lack of suitable and affordable sites for ground-mounted PV forcing successful SDE+ projects to commercial rooftops. Given the small scale of Dutch PV plants, with the largest in the country coming in at only 6 MW, and the high cost of land, ground-mounted projects are uncommon and more expensive to realize than large rooftop arrays. Dutch solar event company Solarplaza reports that the average large-scale PV project size in Holland came in at 1.44 MW by the end of 2015. This is an increase on 790 kW the previous year, but it is still small by global standards. Solarplaza calculates that large-scale capacity has grown from 19.83 MW to 35.9 MW in that period. An additional hurdle for developers is finding a suitable commercial rooftop. While the 2014 SDE+ of €0.14/kWh will be paid for 10 years, a contract must be signed with the building owner to purchase the output of the array beyond the SDE+ period. The government has assumed a spot price of around €0.05/kWh for this period, yet in all likelihood it will be much lower. “A lot of the projects [awarded under the 2014 SDE+] are still not realized because they cannot reach financial close,” says de Werken. Under the SDE+, developers have 12 months after winning a project to contract an EPC and then three years to grid connect the completed array.

In 2016, homegrown solar crowdfunding startup ZonnepanelenDelen (We Share Solar) raised €600,000 in financing required for a 255 kW array at the Volendam Football club. ZonnepanelenDelen cofounder Matthijs Olieman founder says that there is a growing appetite for investing in solar projects from the crowd. The startup aims to raise €2 million this year. ZonnepanelenDelen is expanding its platform so that crowdfunded finance can be provided as loans for residential arrays. However, here a threat to the market exists.

Currently the residential segment is underpinned by the country’s net metering program, which will be in place until 2020. “Next year the government will decide on what will happen with net metering,” says Olieman adding, “2020 is now only a couple of years away and is hanging above the market.” The government has previously subtracted an energy tax of €0.025/kWh, including VAT, to the net metered feed-in. Project developer KiesZon Managing Director Frank Heijckmann says that he expects this year’s review to result in grid connection fees to be additionally deducted from the solar feed-in rate. KiesZon was allocated around 50 MW in the 2015 SDE+ auction, although it too has experienced challenges in realizing many of these projects.

By the midway point of 2016, Holland’s cumulative capacity stood at around 1.3 GW, with Heijckmann and others expecting 400-600 MW in 2016.

Jonathan Gifford

Spain pain for self-consumption

Since April 11, every self-consumption facility in Spain has been subject to the country’s controversial ‘sun tax.’ The regulation was first passed last October but granted six months’ grace for self-consumption PV systems already in operation. Now that period has come to an end, it is compulsory to enter these systems on to the self-consumption facility register and pay the levies established by the new legislation (Royal Decree 900/2015).

Photo: Sofos Energia

Every political party in Spain is against the self-consumption legislation, except the PP (Partido Popular) and the UPN (Unión del Pueblo Navarro). In February, all of the parties bar the PP and UPN signed an agreement committing to amend the self-consumption regulations extensively within their first 100 days in government. Those amendments include exemption from tax on power generated for self-consumption.

Spain’s general election in December failed to produce a government, and a new election has been called for the end of June. This time round, left-wing parties Podemos and Izquierda Unida have made a series of joint proposals, including a National Energy Transition Plan. Not only do the two parties advocate exempting electricity generated for self-consumption from taxation, but also propose that electricity fed into the grid “should be fairly remunerated by electricity suppliers.” At present, many self-consumption facilities are not permitted to sell excess production, meaning that they have to give it away. Self-consumption is currently Spain’s biggest PV market, although there is also some demand for standalone plants. According to the Spanish PV Union (UNEF), last year the sector installed 49 MW of PV. This year, similar capacities are expected.

Blanca Diaz Lopez

Portugal explores large-scale

In Portugal, and according to the latest provisional statistics published by the country’s Directorate-General for Energy and Geology (DGEG), approximately 19 MW of PV were installed in the first two months of this year. That is already just over half of last year’s total (which is around 37 MW). In February the country’s aggregate installed PV capacity stood at 474 MW. Over the course of this year, additional PV capacity of somewhere between 50 MW and 100 MW is possible in Portugal, experts believe. Currently, market growth is mainly driven by self-consumption schemes that were introduced in 2014, as well as initiatives to encourage distributed generation. Under the latter (which is for systems up to 250 kW), operators are paid a tariff established by tender. This year’s awardable power quota totals 19.6 MW. For large-scale PV projects, the European Investment Bank (EIB) this year disclosed that it is considering financing several solar plants in the country. These would comprise a two plant project with a total 100 MW capacity in Alentejo, and a four facility 165 MW initiative developed by Expoentfokus.

Blanca Diaz Lopez

Italy: on the rise again?

At the end of 2015 the IEA released the publication “Snapshot of Global PV Markets.” The IEA data showed that Italy reached 8% (25.2 TWh) penetration for solar PV, which is a higher proportion than any other nation. Broken down further, solar PV in Italy now accounts for approximately 55% of total energy produced from renewable sources, which in 2015 reached 17% of the country’s energy production. As for total capacity installed, cumulatively solar PV in Italy hit the 19 GW mark at the end of 2015. However, despite this ostensibly positive outlook for PV, the IEA noted a sharp reduction in growth, illustrated by a comparison between total capacity installed in 2015 (300 MW) compared to 2014 (a not-immodest 424 MW).

According to IEA’s annual report, Photovoltaic Power Systems Program, the Italian solar sector “has continued to grow, but in a different way than in the past.” This refers to the conclusion in 2013 of Italy’s “Conto Energia,” the feed-in incentive program that had been in place since 2005 and which represented the key driver behind the country’s solar boom. The conclusion of recent installation analysis reveals that the Italian solar market has now reached maturity and needs to identify new opportunities.

Financial incentives, such as the introduction of residential tax relief measures, helped aid the development of the rooftop sector, and will continue to do so throughout the year. This small-scale sector performed better than the medium and large sectors, which failed to grow as expected. Furthermore, the IEA data highlighted another small-scale sector success: Off-grid PV applications grew from almost nothing to 14 MW by the end of 2015.

Today, three years after the end of the FIT program, two provisions are in place aside from tax breaks. The first is net metering (“Scambio sul Posto”), which is considered highly successful. Initially, this scheme was only valid for existing plants with a capacity lower than 200 kW. However, this was later extended in 2015 to incorporate new plants up to 500 kW.

The second is called “Ritiro Dedicato” and refers to electricity sales. This regulation allows GSE to retire the electricity according to an agreement based on minimum tariffs set by the energy authority (Art. 7 AEEG 280/07), or on the market prices that fluctuate depending on the time of the day and region.

However, the legislation for solar is perceived as unstable, and resulted in the 17th edition of Italy’s Solarexpo being postponed until an as yet unspecified date. The event, scheduled for May 3-5, had attracted more than 10,000 professionals from 56 countries in 2015, and its postponement represented a sign of market decline. Despite the measures in place today, the sector lost many producers whom, without financial support coming from the FIT scheme, had to abandon the market because of severe price reductions. Nonetheless the prospects for the sector are positive, explains the IEA: “Thanks to the know-how acquired during the boom years, Italian PV companies are repositioning in foreign markets, providing interesting development for the future growth of this technology.” To this end, Italy’s ENI announced this month its intention to develop a 50 MW solar plant in Pakistan, to be completed by the end of next year. Moreover, thecompany is planning to start operating a solar farm of approximately 150 MW in Egypt. Another two companies, Genesis and Dynkun, signed in April a memorandum of understanding (MoU) with officials from Iran’s northwestern Qazvin province for an array of PV plants totaling, once finished, 1 GW in capacity.

Furthermore, a national project by Eni called “Progetto Italia” involves the development of 220 MW of capacity to be installed in two phases by 2022 on 400 hectares of unused industrial sites across six regions.

As for technological development, the leading actor in the country for research, development and demonstration activities is ENEA. Most of its activity is on materials, cells and PV systems, but focus is also on innovative approaches for the architectural integration of PV elements in buildings and solar concentrator technologies. The IEA reported that in 2015, ENEA began developing and testing emerging technologies and new strategies for integration in the grid on Lampedusa Island, with the scope of addressing value services for users and distributors.

Anna Favero

Greece: FIT again?

Greece’s cumulative PV capacity stands at 2,604 MW, which makes it a significant European PV market. Of this, most was installed in the years 2012 and 2013, while in 2014 and 2015 the country added only 13 MW and 8 MW of new PV systems respectively. Greece had implemented an irrational solar energy policy, which remunerated PV systems with sky-high feed-in tariffs (FITs) leading to projects with internal rates of return up to 40%. Not surprisingly, Greece’s PV subsidy bubble created a deficit, leading to retroactive cuts in 2014.

Photo: Solar Cells Hellas Group

Despite the gloom, there is some good news ahead. According to the EU’s Environmental and Energy State Aid Guidelines (EEAG), from 2016 renewable power generators need to sell their electricity in the market, and member states need to replace their FIT remuneration schemes for the support of renewable energy systems with market premiums.

Greece has not yet implemented a new remuneration scheme following the EEAG guidelines, but the energy ministry published in February a preliminary description of such a scheme, and invited stakeholders to comment on it. According to this, new PV systems up to 500 kW will continue to receive FITs. These are 1.1 times higher than the electricity system’s marginal price, which leads to about €50 per MWh ($56/MWh). Such a tariff, says the Hellenic Association of Photovoltaic Producers (HELAPCO), is not enough to trigger investment. For systems larger than 500 kW, the ministry said competitive tenders alone will define the FITs, with the first tenders expected to start within the first six months of 2016. Therefore, new tenders are expected to be announced by the end of June. There will be at least two tenders in 2016. Furthermore, the new scheme will exclude renewable energy projects on Greek islands that are not interconnected to the mainland’s electricity system. Although the specifics of the tenders have not yet been published, based on the ministry’s preliminary plan, and information published in the Greek press, pv magazine understands the ministry is going to tender about 50 MW of new PV systems larger than 500 kW. Some stakeholders speak of a first tender for projects ranging from 500 kW to 1 MW, and a second tender for projects larger than 1 MW. The same stakeholders said that there will be a cap on the bids of around €90/MWh.

Greece’s energy ministry is preparing an amendment to the net metering legislation to allow for virtual net metering, although this will initally only target specific sectors, such as farming. The existing net metering legislation is sound, but expectations for new net metering PV installations should be kept low due to the restrictions in the flow of capital that the new left wing government imposed last July.

Ilias Tsagas

Austrian aims

The Austrian PV association, Bundesverband Photovoltaic Austria (PVA), expects the PV market to grow by 50 MW in the first quarter of 2016. For the full year, newly installed capacity could amount to as much as 180 MW. The country has a number of different sources of public funding for PV. For small installations with up to 5 kW of capacity, an investment grant is available that covers up to 35% of the total costs. This year, €8.5 million ($9.4 million) has been set aside for this purpose. In addition, systems with capacities of between 5 and 200 kW are eligible to receive a FIT of €0.0824 per kWh. According to PVA, the available budget to mid-December of €8 million has already been depleted. Special investment incentives are available for agricultural and forest product companies in Austria. The budget for this program is xAdvertisement€6.6 million ($7.35 million). Policymakers are also planning major reforms. The Ministry of Economic Affairs is working on a revision of the electricity organization law (ELWOG). The reform would allow PV plants to be used by a number of consumers. Up to now, the use of solar power in multi-tenant buildings or shopping centers in Austria has not been possible. The amendment is expected to the completed by summer.

In addition, lawmakers are considering changing network fees. The PVA says that this change would mean that operators of PV plants who feed excess electricity into the grid would be eligible for an annual compensation payment of up to €30 a year.

Sandra Enkhardt

Switzerland sets its sights

In Switzerland there is an important political decision slated for June that will have a major influence on the further development of the PV market. The government has to decide whether it will increase the surcharge that funds incentives for renewables from CHF 0.013 to a maximum of CHF 0.015/kWh. If the surcharge is raised, it would provide new funding for the second half of the year. If not, the future looks grim for PV incentives.

According to the association Swissolar, between 60 and 70 MW of PV were added in the first quarter. Following the favorable development of the market last year, it is at least holding steady. Operators of PV plants with more than 10 kW capacity can apply for a cost-covering FIT (KEV) or a one-time grant for plants with capacities of up to 30 kW. The funds for the latter incentive are already exhausted, says David Stickelberger of Swissolar. Further plants can only be subsidized if the government raises the KEV surcharge. However, Swissolar does not think that added PV capacity this year will reach more than the 300 MW installed in 2015. “With further funding, we will probably see about 280 MW of installed PV capacity. Without the new funding, the market is likely to stay below the 200 MW mark,” says Stickelberger. He also points to a new trend: Instead of building new plants, operators are opting to expand PV plants that already receive the KEV.

Sandra Enkhardt

Photo: Solar Cells Hellas Group

Britain, solar, and the EU

Brexit or Bremain – that is the question. With Brits set to go to the polls on June 23 to decide whether to stay in or leave the EU, pv magazine asked SolarPower Europe CEO James Watson what kind of impact the vote will have on solar in the U.K. and Europe.

A post-Brexit U.K. solar market may be free from MIP, but given that it is likely to be at least two years before EU treaties no longer apply – by which time MIP could be irrelevant – what is SolarPower Europe’s view, given current price reduction trends in PV?

James Watson: The argument goes that Brexit would be great because the U.K. could have 5% VAT, no MIP on panels coming in from China, thus making the energy transition much cheaper.

Those are short-term arguments. On VAT, the European Commission has already announced that it will bring forward a review package on the VAT directive in 2017, so at the moment there is no pressure on the government to change the VAT rates. Also, MIP is to be decided by the end of this year. The feeling is that we might well be MIP-free by the middle of next year, so this has to be taken into account – the trading situation with China is likely to improve.

They may sound like seductive arguments, but in reality you have to strip it back and ask: Where did solar’s growth in the U.K. come from? The U.K. is now Europe’s third largest PV market in terms of installations. That would never have happened without the Renewable Energy Directive, and that came from the European Commission.

We are currently looking at the 2020-2030 period, which will be crucial for the continued deployment of solar in the U.K., and it is hard to imagine a U.K. outside of the EU doing anything to push solar forward.

Investor confidence is being knocked because of the uncertainty and volatility inherent within the U.K. at the moment. This landscape is not attracting investors, they will go elsewhere. But remember, the U.K. is still in the EU; it’s true that uncertainty is harmful, but it would be worse if the U.K. was outside of the EU because there are no frameworks. Such behavior while still in the EU means there are frameworks for how solar should develop, which will still scare off some investors, but the ability to attract others will remain. The U.K. is in the EU and has still behaved like this. If you are outside of the EU and behave like that, with no overarching framework, it’s going to be worse.

What might the U.K. energy sector look like outside the EU? What kind of relationship could Britain strike with the EU – perhaps something similar to that enjoyed by Norway (which allows it access to the single market but means it has to accept all trade rules, including MIP, and free movement of people) – but if that’s the case, then wouldn’t that make the reasons for Brexit kind of moot?

You can look at the Norwegian model and see Statoil doing well, sending lots of gas down to Europe. They have their hydro, supplying power to Denmark. The U.K. could go a similar way, creating access through interconnections it has with Continental Europe, and Europe wouldn’t want to be without the extra energy the U.K. can provide. So a similar model to Norway’s is possible, but the U.K. will have to abide by certain rules, which means that everything Brexiteers think they are gaining in terms of independence, they are not. The U.K. will simply have to adhere to it.

Another idea is to join the Energy Charter Treaty, which basically ensures that you have a certain commonality in the approach to the EU towards energy policy. The irony here though is that most of the countries that are members of that are accession countries that want to enter the EU and want to harmonize their systems with Europe. It’s a kind of EEA-lite; all that would be happening by joining that treaty is the requirement to basically do what you need to do to trade freely in the energy market with your European counterparts.

So I don’t see much of an alternative from these models, which basically means having to do what the EU wants you to do, but without having a seat at the table.

What about general brain drain? Much of the U.K.’s solar expertise is underpinned by Europeans, many of whom may leave Britain if Brexit happens – is this a concern?

One concern is that the U.K. is the third largest solar market in Europe. There is expertise in U.K.-based companies that want to explore market opportunities in the EU, and these opportunities could be denied them if the U.K. exits the EU. It will be much harder for U.K.-based companies to bring their services and know-how into potential European markets. Poland, for example, could really embrace solar over the next 18 months, and U.K. firms should be well placed to move into that market, but they won’t be able to do that as easily outside of the EU. That is a concern.

The lack of access for British companies that have done well during the U.K. boom in Europe is something that needs to be taken on board by voters. 1 GW of investments could possibly disappear – companies across many markets and sectors have made it clear that if the U.K. is outside of the EU, they don’t see the value of investing in a market of 60 million people, when there is a market of 450 million just next door.

Interview by Ian Clover

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.