A new ranking and rating analysis for the solar photovoltaic (PV) manufacturing ecosystem is released today – the Terawatt PV 100. It reveals the top 100 PV manufacturers, ranked in order from 1 to 100, and rated in bands from Platinum through to Bronze.

Developed by Terawatt PV Research, the analysis uses a new methodology to benchmark component producers (from polysilicon to modules), materials suppliers (from crucibles to glass) and equipment providers (from pullers to stringers) across three key metrics: production scale, financial strength and corporate transparency.

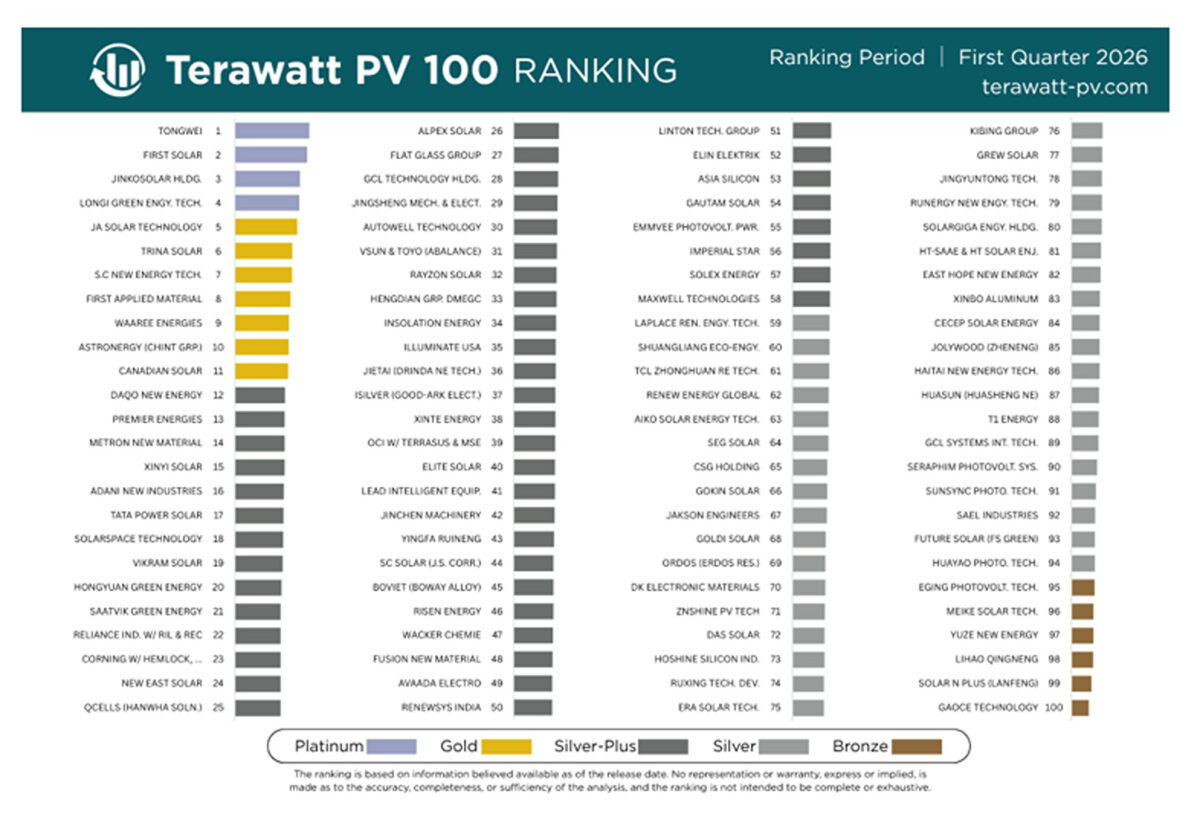

The first-quarter 2026 release places Tongwei as the top ranked company in the solar industry, with the top 100 list containing 21 companies headquartered in India, 12 of the leading companies supplying raw materials and ten companies focused on producing equipment.

Companies headquartered in China account for almost 60% of the top 100, with First Solar and Waaree the only non-Chinese based inclusions in the top 10.

S.C New Energy occupies the highest ranking for an equipment provider, with First Applied the leading materials supplier.

Four companies achieve the highest Platinum rating (Tongwei, First Solar, Jinko Solar and Longi), with seven companies having Gold rating status: JA Solar, Trina Solar, S.C New Energy, First Applied, Waaree, Astronergy and Canadian Solar.

This article introduces the Terawatt PV 100 rankings and the background to the underlying analysis. It explains why the PV sector is demanding a greater level of scrutiny today on companies across the entire manufacturing ecosystem. The methodology developed to analyse and benchmark the leading manufacturers in this space is then outlined. And finally, some of the key findings at the company level arising from the first-quarter 2026 release are presented.

US solar tariffs and global ESG mandates force supply-chain scrutiny

During the early growth phase of the PV industry, module procurement was often influenced by pricing and availability issues, particularly when supply was tight or delivery dates were critical.

This changed in 2012 when the U.S. Department of Commerce imposed antidumping and countervailing duties (AD/CVD) on silicon-based cells manufactured in China, known as “Solar 1”; and subsequently followed up by Solar II in 2015 (covering silicon-based modules assembled in China), Solar III in 2024 (relating to cells produced in Cambodia, Malaysia, Thailand and Vietnam) and Solar IV in 2026 (expanding to Indonesia, Laos and India).

Over the past decade, these cases have compelled the U.S. module buying community to understand fully the country of origin for silicon-based manufacturing.

While Solar I-IV created a geographic filter to dictate tariff-free supply options, the U.S. Uyghur Forced Labor Prevention Act (UFLPA) in 2022 added a new dimension, forcing U.S. module buyers to trace supply-chains back to polysilicon.

While the new buying culture in the United States was created largely from a legislative standpoint, by the early 2020s there was a greater transition happening globally towards Environmental, Social, and Governance (ESG) mandates. Ultimately, this put solar supply-chain scrutiny onto the global stage for the first time.

But how much is known about the companies in the solar manufacturing supply-chain? And should the scrutiny be confined to producers across the value-chain, making polysilicon, ingots, wafers, cells and modules – or include the materials suppliers and equipment providers?

Currently, the direction of travel is towards greater value-chain and supply-chain scrutiny. Not simply the location of corporate headquarters, nor the percentage of shareholding attributed to citizens of a specific country. But to understand the business models of these companies, their technology roadmaps, production volumes, market-share trends, financial health metrics and corporate transparency levels.

Analysing the entire PV manufacturing ecosystem

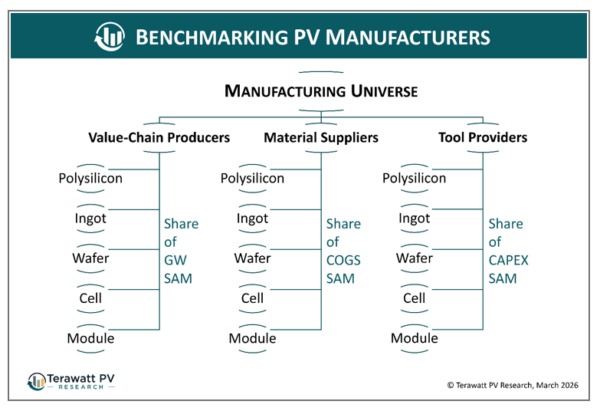

The methodology underpinning the Terawatt PV 100 ranking list is based on scoring each company across three categories: production scale, financial strength and corporate transparency.

Production scale scoring for companies manufacturing different products has not been undertaken before in the PV industry. To achieve this, the PV manufacturing ecosystem is treated as a single, total addressable market (TAM), within which all companies compete; producers of key components across the value-chain (such as wafers or cells), suppliers of materials (such as silver paste or backsheets) and equipment providers.

Each of these company types (producers, suppliers and providers) competes in specific served addressable markets (SAMs), dictated by the production volumes each quarter/year (for the component producers), the raw materials contributions to the cost-of-goods-sold or COGS (for the materials suppliers), and the factory capital expenditure or capex (for the equipment providers).

This allows a production score to be generated for any manufacturer, with contributions from different SAMs additive. For example, companies making wafers, cells and modules have contributions from three different stages of the value-chain; similarly for companies producing diamond wire saws (equipment) and diamond wires (materials).

By default, the companies with the greatest market share within any individual SAM (for example, cell production or solar glass supply) see the largest production scale contributions.

The financial strength analysis is less nuanced compared to the production scale scoring. The challenge here was to devise a robust methodology that was tailored to the solar industry, not simply defaulting to prescribed models that may not capture the true fortunes of solar industry participants.

The choice of accounting ratios to extract for each company was done by examining a host of liquidity and debt metrics from the sample set (more than 150 companies going back to 2020), reflecting near-term (12-month outlook) and long-term operations.

The focus on this subset of accounting ratios was intentional. Most solar manufacturers are heavily dependent on revenues from just one or two products, specific to the solar industry. As such, cash-flow and debt become the two issues to manage, with solar being a technology sector that inevitably goes through unforeseen, and often severe, upturns and downturns.

In addition to the four financial ratios covering liquidity and debt across near- and long-term periods, a new metric was incorporated to allow final financial scores for each company to be determined. This addressed the “outliers” that have always existed in the PV industry; companies whose PV operations represent a small percentage of overall group turnover.

Examples here go back to the early days of solar PV manufacturing, such as Sharp, Mitsubishi, Kyocera, LG Electronics, and Samsung. And today, the list contains the likes of Hyundai, Hanwha, Adani, Reliance and Tata.

Solar manufacturing business units which are part of these “conglomerates” are typically less exposed to cycles in PV sector prosperity, compared to smaller pure-play manufacturers. And often the solar business units of the larger entities can be run comfortably for extended periods of loss-making, if there is a greater strategic value in sustaining a manufacturing presence in the solar industry.

Therefore, an extra contribution was considered when benchmarking companies in the PV manufacturing ecosystem – a “parent security” metric. In effect, an uplift factor that protects the PV business operations of conglomerates from any periods of prolonged solar loss-making.

The final input to the overall company scores is the most qualitative in nature, based on a new performance metric covering social governance (including ESG reporting), supply-chain visibility, clarity in corporate ownership status and operational transparency. These factors are folded into the third scoring factor, called “corporate transparency”.

The focus on corporate transparency addresses the growing trend of companies to be accountable in operations to the outside world, with the days of existing in “stealth” mode largely being confined to the past.

The final scores are obtained by weighted contributions from the three pillars: production scale, financial strength and corporate transparency. A minimum production level is used for each of the manufacturing categories (component producers, materials suppliers and equipment providers) to prevent erroneous inclusion of low-volume producers.

The top 100 companies are then ranked by score, while also being grouped into ratings bands. The ratings are derived purely from a Z-score analysis, categorizing companies by their standard deviation from the mean to provide a statistically objective measure of relative performance.

Platinum rating is assigned to companies with Z > 2, Gold at Z > 1, Silver-plus for Z > 0, Silver for Z > -1 and Bronze for Z < -1.

The mean and standard deviation is calculated from the complete data set for more than 150 companies between the start of 2020 and first-quarter 2026. This inclusion of historic values is important. Since 2020, the PV sector has been through extreme levels of upturn and downturn, allowing a full distribution dataset to be used as the statistical anchor. Also, going back in time before 2020 would have included data that was generated from a PV sector still moving out its early-growth status.

Accordingly, ranking levels and rating bands for any given quarter are relative to the extremes of performance seen since 2020. This provides one of the major differentiators of the new methodology where entire segments of the ecosystem can see rankings and ratings decline when the sector is subject to downturn or recession characteristics.

Key findings from the Q1 2026 release

The Terawatt PV 100 ranking list is dominated by value-chain component manufacturers, with the leading polysilicon, ingot, wafer, cell and module producers all featuring strongly. Companies making more than one component in the value-chain command the highest production scale contributions, with the financial strength and corporate transparency metrics then providing a final ranking position.

Value-chain manufacturers by default feature most prominently, compared to other materials or equipment suppliers that often supply just one product within their company’s specific SAMs. For example, an equipment supplier offering only a laminator as part of overall module capex will typically have a production score well below a leading supplier of turn-key module lines.

However, within the materials and equipment segments, some of the companies command very high market share and, as such, feature prominently in the rankings.

The two leading glass suppliers in the industry, Flat Glass Group and Xinyi, are listed in the top 30. The dominant supplier of diamond wires, Metron New Materials, is in the top 15. The market leader in cell production equipment, S.C New Energy is in the top 10. The leading supplier of module films and backsheets, First Applied, also features in the top 10.

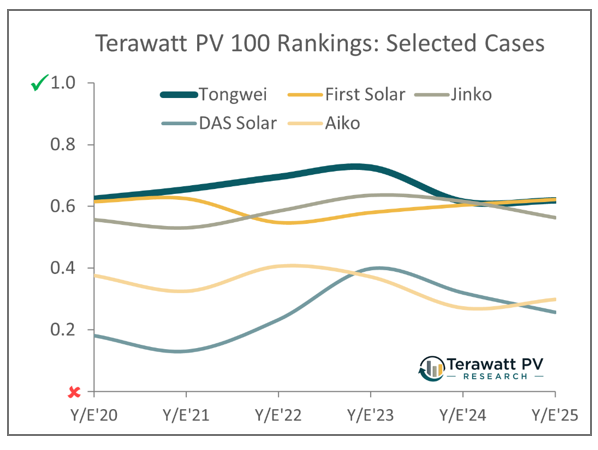

Across the entire top 100, Tongwei and First Solar are the clear leaders today, with Tongwei only marginally ahead for the first-quarter 2026 listing.

Tongwei’s position at the top is driven largely by its leading production status today for polysilicon and cells, with meaningful additions from its growing module production activities. The company also scores high for corporate transparency as one of the first Chinese companies to embrace voluntary disclosure of English-facing documentation. However, Tongwei’s overall Terawatt PV 100 scores have been in decline since 2023 with one of the key contributors to financial health (short-term profitability) falling by more than 50% during 2024 and 2025.

In contrast to most Chinese producers, First Solar’s overall score has increased since 2022; a reflection of how the second PV manufacturing downturn has been largely confined to Chinese companies.

First Solar’s high-ranking position has a more balanced set of contributing scores, with the company industry-leading for corporate transparency, in the top few for financial strength and with strong production scores owning to the company’s thin-film technology effectively having a full value-chain coverage when harmonized with silicon-based manufacturing.

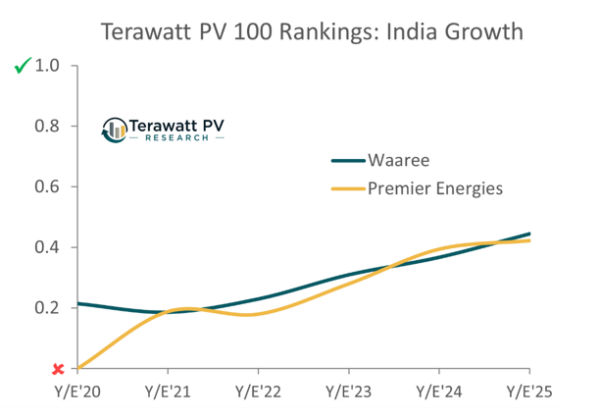

However, the key takeaway is the inclusion of 21 Indian companies in the top 100. This includes well-known conglomerates (Adani, Reliance and Tata) and companies that have been exposed to the global PV sector in the past (such as Waaree, Premier Energies and Vikram).

Moreover, some of the Indian companies included are largely unknown outside India today, having expanded module capacity in the past 12-18 months as the domestic sector warmed to the favourable pricing environment on offer. This includes companies such as Alpex, Avaada, Insolation Energy and SAEL Industries.

Within this full list of 21 Indian companies featured, Waaree and Premier Energies show the greatest growth trajectories in the rankings, when comparing positions held by these companies in first-quarter 2026 to levels seen back in 2020.

What to expect during 2026

In contrast to most other PV sector rankings or ratings that often show little, if any, changes even on an annual basis, the Terawatt PV 100 methodology is designed by nature to be a highly dynamic tool. Even on a quarterly basis, significant changes can occur in positions, with many of the companies closely ranked across the dominant Silver-plus and Silver ratings bands.

When the second-quarter 2026 ranking list is released in June, many of the Chinese companies in the lower bands may see strong downward adjustments, particularly if decisions are made in the first half of the year to wind-down PV operations or scale back value-chain production volumes through enforced asset disposal or debt restructuring.

The next ranking list is also expected to see a further 5-10 Indian companies included, given the sheer volume of new entrants in the past 6-9 months ramping up module factories with 2-5 GW of capacity installed.

The final category to monitor will be the PV equipment suppliers, some of whom are sustaining first-quarter 2026 inclusion by virtue of delayed revenue-recognition from tool shipments as far back as 2023.

The full analysis of all top 100 companies shown in the rankings is covered in detail in the first release of the new Terawatt PV 100 Quarterly report, providing insights into company ownership status, manufacturing footprints, subsidiary operations, controlling shareholders, production and technology metrics, supply-chains, key customers, corporate transparency activity and a critique on company strategy and risk factors. Details on accessing the report are provided by Terawatt PV Research.

Finlay Colville has been actively engaged with the solar industry for more than 20 years and is recognized as a leading analyst in the sector. With a focus on technology, manufacturing and corporate strategy, he has devised some of the industry’s most successful market reports and technical conferences. Finlay has written more than 750 feature articles and delivered more than 500 presentations, in addition to consulting arrangements with over 100 companies. In 2023, he was awarded the Solar & Storage Live ‘Lifetime Achievement Award’. For 15 years, Finlay managed the market research business units at Solarbuzz and PV-Tech. He established Terawatt PV Research in 2025 for his activities going forward.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.