Trading activity in the global polysilicon market remained subdued this week. OPIS learnt that a limited number of spot transactions are currently under negotiation, which could result in a marginal upward adjustment in prices, according to industry sources.

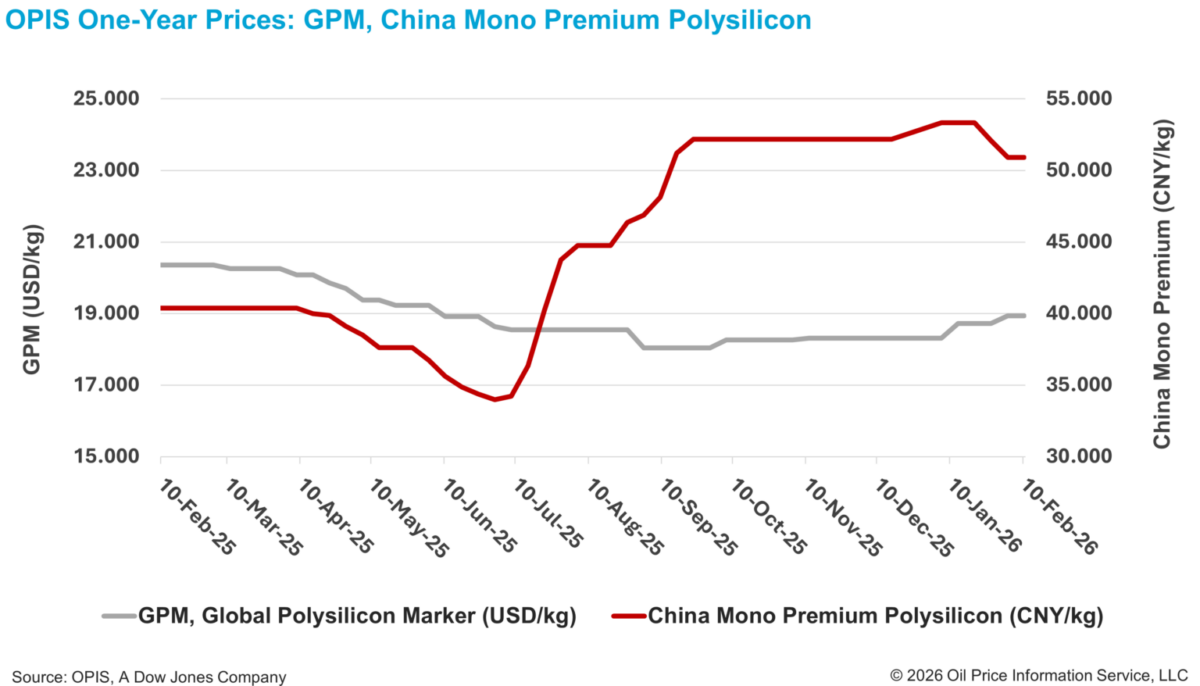

According to the OPIS Global Solar Markets Report released on February 10, the Global Polysilicon Marker (GPM)—the OPIS benchmark for polysilicon produced outside China—was assessed at $18.942/kg, or $0.040/W, remaining unchanged from the previous week.

This followed a 1.14% increase the prior week, driven by reports of one manufacturer implementing a modest price increase, though higher levels have not been widely accepted by downstream buyers.

Market participants indicated that the manufacturer’s pricing decision reflects “optimistic” expectations regarding the outcome of the U.S. Section 232 national security investigation into polysilicon and its derivatives. In particular, the market anticipates that certain tariff exemptions may be granted to long-term partners and allied countries, supporting a more bullish outlook for non-U.S.-produced polysilicon.

Despite this optimism, market observers caution that the potential outcomes of Section 232 present a double-edged sword for non-U.S. polysilicon producers. While volumes qualifying for duty-free quotas could benefit from higher prices and improved demand, production capacity falling outside these exemptions may face significant pressure on both pricing and offtake.

On the supply side, a new polysilicon facility in Oman with a nominal annual capacity of 100,000 metric tons (MT) commenced operations last week. Industry participants noted that while the commencement of this Omani facility could have some impact on the global polysilicon market, the near-term effect is likely to be limited. One insider noted that it typically takes at least three months from initial production for product quality to stabilize, and that beyond quality, a range of operational, logistical, and commercial factors must be addressed between buyers and sellers, requiring careful, case-by-case coordination.

Similarly, trading activity in the Chinese polysilicon market was largely stagnant this week. Market participants attributed the lack of transactions primarily to uncertainty surrounding market conditions going forward, as well as unclear operating rates among downstream manufacturers, which has significantly reduced buyers’ urgency to procure polysilicon.

The China Mono Premium—OPIS’ assessment for mono-grade polysilicon used in n-type ingot production—was unchanged week-on-week at CNY 50.917 ($7.38)/kg, or CNY 0.107/W.

Polysilicon suppliers—particularly leading producers—continue to prioritize price stability, a stance that has, to some extent, further dampened purchasing interest, according to a market participant.

Industry sources also noted that while some manufacturers have marginally increased output following production line adjustments, shutdowns and production curtailments at major facilities have led to a meaningful reduction in overall market supply. This supply contraction is one of the key factors underpinning major producers’ efforts to maintain prices.

Data from the Silicon Branch of the China Nonferrous Metals Industry Association (CNMIA) show that China’s polysilicon output in January totaled approximately 102,000 MT, down 8.3% month on month. In February, CNMIA expects production to decline to around 85,000 MT while estimating demand from wafer producers at about 80,000 MT, suggesting that the pace of inventory accumulation is slowing.

Another market participant said polysilicon prices are expected to remain at depressed levels, below CNY 55/kg, for an extended period, potentially through 2026. The source added that reductions in operating rates do not equate to a meaningful exit of excess capacity, and that industry consolidation remains necessary, although the pathway and timing for such consolidation remain uncertain.

OPIS, a Dow Jones company, provides energy prices, news, data, and analysis on gasoline, diesel, jet fuel, LPG/NGL, coal, metals, and chemicals, as well as renewable fuels and environmental commodities. It acquired pricing data assets from Singapore Solar Exchange in 2022 and now publishes the OPIS APAC Solar Weekly Report.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.