Alberta-based Enverus Intelligence Research (EIR) projects that expected increases in U.S. energy demand combined with federal policy changes and delays in interconnection queues are tightening the economics of renewable energy projects, particularly solar. As a result, developers have to make new cases for keeping solar a major player in the generation mix going forward.

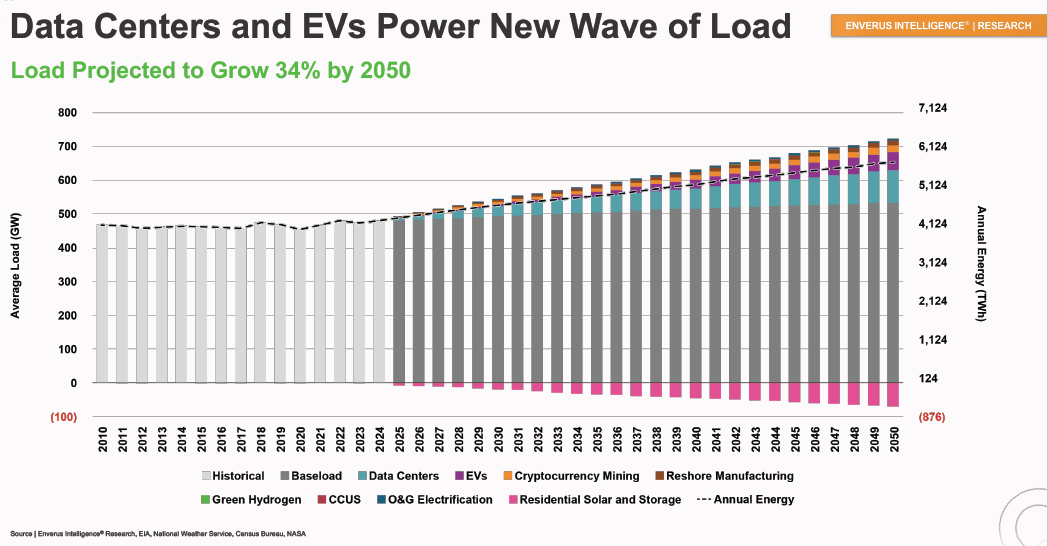

A new EIR report says projects U.S. electricity demand will rise 34% by 2050, intensifying the need for reliable generation as data centers, electrification and industrial load growth outpace new capacity additions. As a result, U.S. power market is no longer optimizing for lowest marginal cost but is optimizing for reliability.

Other significant conclusions from the report include the following:

- Interconnection delays now average 3.5 years, creating a structural bottleneck that slows renewable buildouts and elevates near term supply risk across multiple independent system operators (ISOs);

- Renewable energy economics are under mounting pressure as accelerated tax credit retirements, new tariffs and foreign entity of concern (FEOC) requirements push levelized cost of energy (LCOE) higher, with impacts varying significantly by region;

- Solar transaction valuations fell sharply in 2025, with average deal multiples dropping to roughly half of the ~$1 million per megawatt levels observed since late 2024, reflecting tighter economics and policy uncertainty; and

- Battery energy storage retains federal tax credit support, but market saturation, lower price volatility and compliance uncertainty are narrowing opportunities, making regional selectivity increasingly critical.

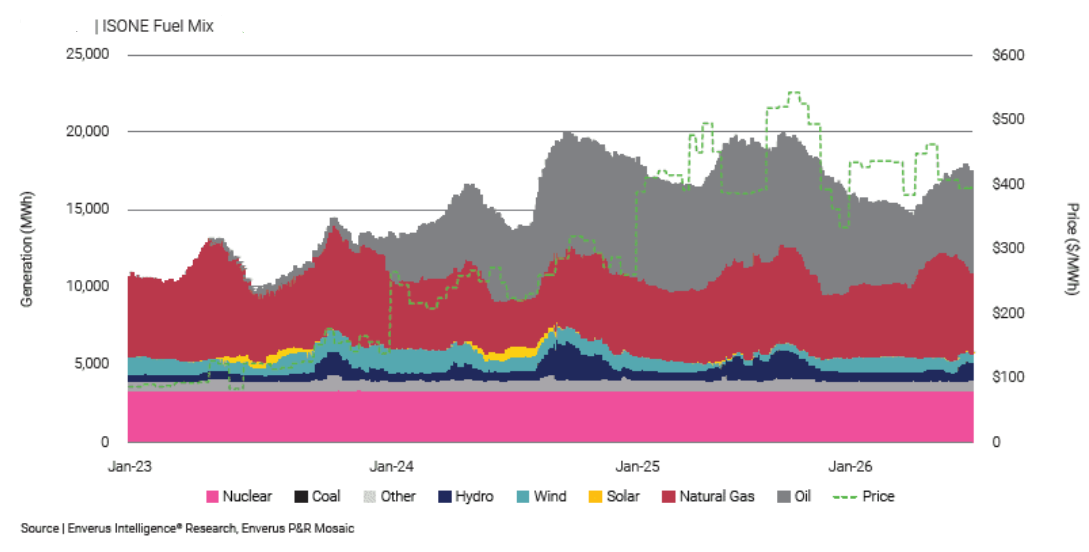

According EIR analysts, extreme weather events such as the recent winter storm in the Northeast and Midwest intensify the pressure on renewables, revealing their limitations at providing dispatchable power during periods of peak demand. In January, for example, solar-forward and natural gas-constrained states such as New York and Massachusetts largely turned to oil to keep the heat and lights on.

Another new Enverus report reads: “During peak cold conditions, oil and dual-fuel generation rose sharply across Northeast power markets, reaching 44% of total generation in the New York Independent System Operator (NYISO) and approximately 35% of output in ISO New England (ISO-NE), as natural gas infrastructure operated at or near full capacity and fuel flexibility narrowed.”

Juan Arteaga, principal analyst at EIR, told pv magazine USA that solar wasn’t generating enough in the Northeast during the storm and the ISOs couldn’t get any more gas. “So, the mentality now is, keep the lights on,” he said. “They don’t care as much where the electricity is coming from. That’s the reality.”

This is very much a regional issue, and performance depends on the availability of the solar resource. Certain affected regions, such as Texas, weathered the storm better with grid batteries and more renewable generation under less severe conditions. Last fall, Enverus reported that the Electric Reliability Council of Texas (ERCOT) service area is awash in battery based energy storage system (BESS) capacity that while reducing revenues for ancillary services does provide dispatchable power during peak demand as intended.

All-in-all, Arteaga said, the demand forecasts are causing once sluggish ISOs to fast-track dispatchable generation in their queues.

“They’re pushing,” he said. “They’re pretty much accelerating the queue process, or in some cases just skipping it, for a number of projects that they deem as necessary, mainly gas projects. And they’re pushing them through much faster to get them online before 2030.”

Sauce for the goose is sauce for the gander, and if demand is lengthening the wait times to get solar interconnection, it is also imposing limitations on access to combined-cycle gas turbine generators. Just as you can only manage so many interconnections at a time, you can only get your hands on so much essential equipment for a project.

“We’ve been hearing is that you cannot even put an order in for any new gas turbine before 2030,” Arteaga said. “There’s a huge supply chain constraint there. The manufacturers are at capacity and pretty much just producing the orders that they have in the backlog.”

Herin lies the opportunity for renewable energy developers and the industry as a whole. If policies are raising solar’s LCOE, the primacy of demand makes this less of an issue if solar-plus-BESS is reliably dispatchable. If interconnection queues are an issue, some developers are exploring behind-the-meter generation, essentially building GW-scale microgrids to meet demand. Also, some manufacturers are responding to FEOC requirements by bringing more PV module and balance of system manufacturing into the United States.

The research that shows load increases out to the horizon means that reliable capacity will always be in demand. Demand may be changing priorities, but the case for solar remains strong if the industry adapts to them.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.