From pv magazine 6/25 – The Hunt For High Efficiency

Increasingly fractious trade relations have led to divergent price spreads in key markets. Compared with free on board (FOB) China tunnel oxide passivated contact (TOPCon) modules, those delivered duty paid (DDP) to the United States were trading at a premium of around $0.18/W as of May 20, according to OPIS analysis. This was down on the $0.195/W premium recorded at the start of the year. On the same comparison basis, DDP Europe modules were trading a premium of $0.03/W, compared to $0.016/W in January.

Uncertainty around the future of tax and investment incentives is denting module demand and capping module prices in the United States. Developers are holding back on purchases due to nervousness among financiers concerned about the future availability of tax credits introduced by the previous U.S. administration. Europe, meanwhile, remains one of the key markets where Chinese modules are aggressively competing.

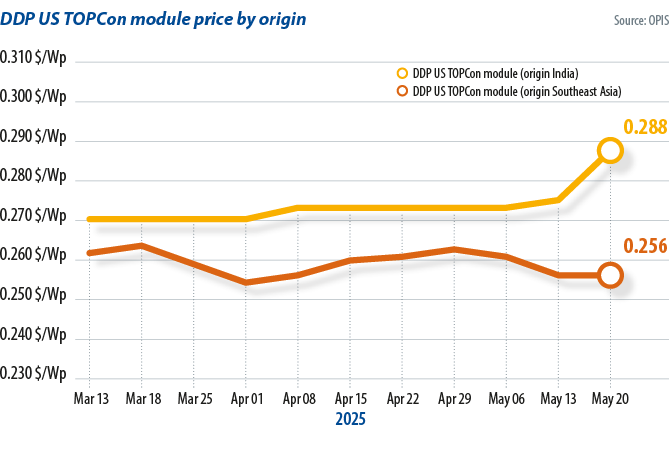

Even within the DDP U.S. market, there are signs of increasing price fragmentation. The price of Southeast Asian imports at the start of March 2025, namely from Indonesia and Laos, was trading at a $0.007/W discount compared to Indian imports on a DDP U.S. basis. But this spread later widened to $0.032/W on May 20, with Indian cargoes assessed at $0.288/W and Southeast Asian cargoes at $0.256/W.

Tariff risks

Tariff risks, real or perceived, remain the biggest price mover in the DDP U.S. market. Company-specific antidumping and countervailing duties (AD/CVD) have seen most Southeast Asian modules excluded from the U.S. import market since late 2024, except those from Indonesia and Laos, which have so far dodged the brunt of U.S. trade policies.

But concerns remain that AD/CVD would be applied to more Southeast Asian imports. A general oversupply in Southeast Asia’s solar market also persists, capping offer prices even for modules from Indonesia and Laos. India, meanwhile, is building out its own solar supply chain that could result in far fewer trade hurdles for its module exports into the DDP US market, but the country has its own fast-growing domestic demand for locally made modules to fulfill. These contrasting dynamics look set to drive the price fragmentation in the DDP U.S. market over the short and medium term.

Further upstream, cell prices have dipped back to levels seen at the end of 2024, following a slight recovery. OPIS assessed the price of FOB China TOPCon M10 cells at $0.035/W on May 20, after hitting a year-to-date high of $0.039/W on April 15. Chinese cell production was high from March through April, according to an OPIS survey. Leading manufacturers utilized over 70% of their production capacity, while second- and third-tier producers maintained levels around 50% capacity utilization.

The outlook for May has deteriorated. Top-tier manufacturers are expected to reduce utilization rates to below 60%, while smaller players may drop below 30%. Sources report that projected production has been revised down from 64 GW in April to about 58 GW in May, with further cuts likely amid continued downstream weakness.

Future trends

Looking ahead, industry sources suggest pricing trends may diverge across different n-type cell specifications. Chinese cell producers are reportedly shifting focus toward rectangular “210R” cells measuring 182 mm x 210 mm. This could increase supply and exert additional downward pressure on prices for this specification.

The Global Polysilicon Marker (GPM), the OPIS benchmark for polysilicon produced outside of China, continued to decline amid market pessimism, falling to $19.233/kg on May 20, a four-year low.

Contrary to expectations, the three-month suspension of new US tariffs failed to significantly stimulate wafer production in Southeast Asia, dashing hopes for a short-term boost in non-Chinese polysilicon demand.

Wafer production levels in Southeast Asia are enough to support the limited solar cell output currently eligible for export to the United States, according to a major integrated manufacturer. That output is concentrated in a handful of countries.

Major polysilicon manufacturers in China reportedly plan to maintain low operating rates, utilizing around 40% of production capacity. The upcoming rainy season will bring a fall in hydropower-based electricity prices, which should boost production in the Sichuan and Yunnan regions. Manufacturers are expected to carry out plant maintenance to manage total production levels.

About the author

Hanwei Wu, the editorial director of OPIS, leads the Asia-Pacific team in producing price assessments, proprietary data, and news analysis for the solar, carbon, oil, and petrochemical markets. In recent years he has launched data products for the oil and renewables markets, including solar.

Hanwei Wu, the editorial director of OPIS, leads the Asia-Pacific team in producing price assessments, proprietary data, and news analysis for the solar, carbon, oil, and petrochemical markets. In recent years he has launched data products for the oil and renewables markets, including solar.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.