A growing number of PV module manufacturers are threatening to shut down their production facilities in Europe due to the ongoing low-price trend. Some want to give up, while others want to move to the United States, where there are supposedly better market and funding conditions.

That’s not entirely wrong, because current module prices in Europe do not reflect a healthy, industry-friendly market situation. On the contrary, price levels are still dominated by warehouse clearance sales on a large scale.

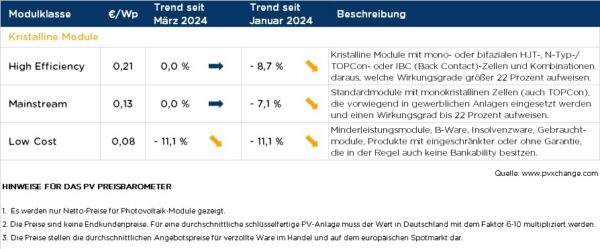

This month, module prices no longer fell across the board. However, recovery to a level at which newly produced products in Europe can be offered competitively seems unattainable in the long term.

There is still too much stock left among distributors and manufacturers for second-tier or third-tier products. Due to the recent cold temperatures, demand has not yet returned to the levels expected for this time of year, so excess modules are only flowing out slowly.

The prices currently circulating in the photovoltaic market for passivated emitter and rear cell (PERC) products under 2 square meters up to 410 W are just under €0.10 ($10.66)/W, so they were assigned to the “low-cost” price point this month. This is basically the reason for additional declines in the price index.

Higher performance classes, as well as full-black and glass-glass modules, were still assigned to the “mainstream” or “high-efficiency” group, as these products can still be sold reasonably, although they offer lower performance. Only standard modules of around 400 W are increasingly becoming slow sellers and are often sold off with all possible force – there is no foreseeable lower price limit there.

To make matters worse, the elimination of a customs exemption for bifacial glass-glass modules is now being discussed in the United States. The reason is probably a request from Hanwha Qcells to the Department of Commerce in order not to endanger the planned expansion of production on the North American continent. If this petition is successful, the prices of non-Chinese modules in the United States will also increase significantly. Chinese modules will hardly find their way into the US market and, as a result, they will probably end up in Europe and further increase the pressure on already low module prices.

If local production is to remain in Europe in the foreseeable future, policymakers will really have to come up with something suddenly. Even if it won’t be a resilience bonus like the one recently scrapped in Germany, the course should be set in the right direction as quickly as possible – preferably at the European level. Currently, every day that no action is taken, a small part of our independence in the energy sector dies.

Price points differentiated by technology in April 2024, including changes from the previous month (as of April 20, 2024):

About the author: Martin Schachinger studied electrical engineering and has been active in the field of photovoltaics and renewable energy for almost 30 years. In 2004, he set up a business, founding the pvXchange.com online trading platform. The company stocks standard components for new installations and solar modules and inverters that are no longer being produced.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

$10.66 per watt?

You bungled $ with ¢ badly.

€0.10 = $0.1066 = 10.66¢ as there are 100 cents in a dollar, $1.00 = 100¢.

When you wrote “ €0.10 ($10.66)/W” you mixed up cents ¢ with dollars $ and multiplied by a factor of 100.

Please correct. It should read “ €0.10 (10.66¢)/W” or “ €0.10 ($0.1066)/W.”