There is no company that quite represents the contradictions in the solar industry as much as SunPower. The Silicon Valley-headquartered company makes the highest efficiency solar products available on the mass market, and has gained an enviable market share in the rooftop solar market, but still struggles to turn a quarterly profit.

Q4 2018 was no exception. While the company’s losses in the second half 2018 were greatly reduced from prior quarters – likely due to its substantial restructuring – the company still reported a net loss of $172 million on $457 million in revenues.

Nor is there necessarily and end in sight. After missing its pledge to return to profitability in the second half of 2018, SunPower deferred this question to an investor day on March 27.

Fortunately for SunPower, majority owner Total appears to be playing the long game; and there were ample successes to celebrate in SunPower’s results. Also, even while reporting losses SunPower managed to reduce its debt substantially during the quarter with proceeds from the securitization of its loan assets and the sale of its microinverter business.

DG market share gains

Part of SunPower’s restructuring has included abandoning its utility-scale solar development business and focusing on where its technology offers the greatest benefits – on rooftops and other distributed applications. And here SunPower is shining.

SunPower closed 2018 claiming a leading position in the highly fragmented U.S. commercial and industrial market, with 49 MW installed during Q4. Much of this is on the back of big customers like Walmart, which had the 2nd-highest volume of on-site solar deployed of any U.S. corporation at the end of 2017.

But it is the company’s residential business which is even more impressive. During the fourth quarter SunPower deployed 75 MW of residential solar, which is more than Tesla’s 73 MW of combined residential and C&I, and could position the company as the 2nd-largest company in the residential solar space after Sunrun.

It is important to note that SunPower does not have in-house installation crews, and instead depends on a network of installers who use its products, including its modules, Equinox system and loan products. As such this 2nd place represents the aggregate work of many installation companies nationally.

Regardless, this is remarkable growth, and notably SunPower grew its residential installations 15% in 2018, despite flat market growth overall- meaning that it is gaining share as former leaders like Tesla and Vivint become less dominant.

And this may only be the beginning. SunPower claims a leading market share in the new home market, and while this market only made up an estimated 10-15% of its residential sales during Q4, the new homes business is poised to get much bigger when California’s mandate for solar on new homes kicks in.

This could be particularly good for SunPower’s bottom line; as we at pv magazine USA have explored, the elimination of sales and much of the installation cost plus raw economies of scale mean that solar can be installed much more cheaply on new homes, leaving more room for manufacturing margins.

NGT comes online

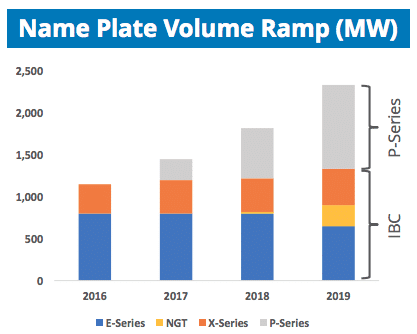

SunPower’s market share gains are not the only thing it celebrated on its Q4 call. The company also began production of its Next Generation Technology (NGT) product at one of its lines at its Fab 3 in Malaysia.

NGT is a lower-cost version of SunPower’s Interdigitated Back Contact (IBC) solar technology, which SunPower says is made possible through both improved manufacturing efficiencies and throughput as well as the use of larger wafers. “On some tools we figured out how to double the throughput,” SunPower CEO Tom Werner told pv magazine.

There’s no data sheet yet to show off the NGT modules, but Werner says that the product will be formally unveiled in coming weeks at an installer conference. Regardless, SunPower is planning to put on another line of NGT by the end of the year to reach 250 MW of annual manufacturing capacity.

Graphic: SunPower

This plus the ramping of SunPower’s P-Series production at the former SolarWorld factory in Oregon mean that the company will be strongly diversified from its legacy E-Series and X-Series with less expensive products. However the efficiencies are still high; the mono-PERC P-Series produced in Oregon is 19% efficient.

Margins remain tight; a gross margin above 18% for the company’s residential business managed to offset losses in its manufacturing division during the year, as C&I came in at 9% gross margin. It remains to be seen when SunPower will translate its remarkable technical and market successes into quarterly profits. In the interim, the company is still a leader – even while in the red.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

Hi Christian: You always write thought-provoking articles and this is no exception. In the first paragraph you write: “The Silicon Valley-headquartered company makes the highest efficiency solar products available on the mass market……….”

What is the percentage of photons to DC electricity conversion factor of SUN POWER PV cells?

Thank you for your valuable time Christian Roselund

Thank you.

It depends on the product. For the Maxeon cells used in E-Series and X-Series, they’ve gotten up to 24%, but at the module level the average panel efficiency of their best model is at 21.5%. For the P-Series made in Oregon, the module efficiency is 19%.

I WANT TO SEE A WORLD MORE CLEAN THIS IS WONDERFULL THANK YOU FOR WORLD MORE CLEAN.I LIVING IN BRAZIL.MY NAME IS ENYO.

SunPower X22-370W – 22,7%!!

Sunpower Maxeon 327w X20 @ 20.0% efficiency