There has been great speculation regarding how much potential U.S. trade action imported PV cells and modules will effect the U.S. market. And while pv magazine has been hearing stories about module price increases for at least four months, there have been few formal analyses of how much prices have increased and how this has affected system prices.

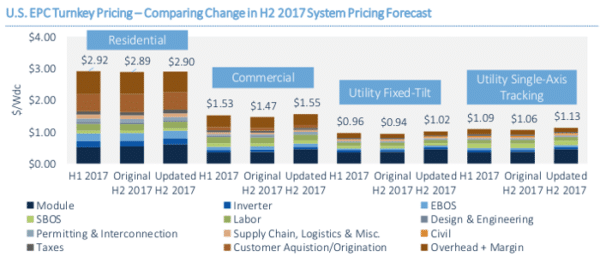

That is, until today. GTM Research has released an analysis which estimates that along with a roughly 5 cent per watt increase in module prices, that system costs in the second half of 2017 have risen by as much as 6% for fixed-tilt utility-scale solar costs. The company notes that this is the first time in recent memory that system prices have gone up, instead of down, on a half-year basis.

The potential impact of solar tariffs in twelve charts shows price increases in the commercial and industrial sector and for utility-scale systems with tracking as well, with residential solar pricing relatively unaffected.

An important detail here is GTM Research has found that prices for small-scale procurement in the United States are deviating from global prices, which continue a slow, steady decline.

Different scenarios

Another important aspect of this report is that GTM Research, for the first time, has modeled what different tariff levels look like for the U.S. market. The company notes that steeper tariffs would have a disproportionate impact on the market, estimating that a $0.10 per watt module tariff would decrease demand 9% from its base case scenario, whereas a $0.40 per watt tariff would mean a 48% decrease.

Neither of these lines up exactly with what the petitioners are asking for, however the International Trade Commission (ITC) is not bound to follow the petitioner’s request, nor is the Trump Administration bound by either the request nor the ITC’s recommendations.

Again, the utility-scale segment is likely to be the hardest hit by higher tariff levels, with GTM Research estimating at 57% decline in this segment at a $0.40 cent per watt module tariff. This is for two reasons. First, modules represent a larger portion of the overall costs of utility-scale systems, and second because utility-scale solar competes directly with other sources of energy, most notably natural gas.

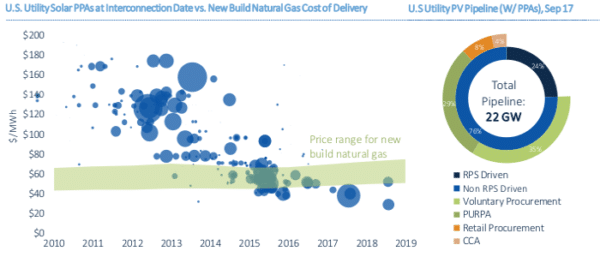

GTM Research notes that for the first time since 2015-2016, solar plants going online were coming in at the same price as new-build natural gas projects. And since 76% of the utility-scale solar pipeline identified by the company is not driven by renewable energy mandates, any increase in price endangers this market segment.

A core consideration here is how much module supply will be available on a tariff-free basis. GTM Research has found 4.8 GW of cells and 6.7 GW of module capacity either from thin-film solar, U.S. production or manufacturing in nations that are not subject to tariffs.

The biggest two potential sources of non-U.S. production are First Solar’s factory in Malaysia and REC Solar’s Singapore production. U.S. cell production was estimated at 1.5 GW in 2018.

As the petitioners are calling for tariffs on cells as well, tariff-free supply will likely be limited to around 5 GW. Adding the 2 GW of modules that GTM Research estimates have already been procured for 2018 projects gives the 2018 market a ceiling of 6.9 GW under the use of tariff-free modules, however GTM Research indicates that actual available volume will likely be lower.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.