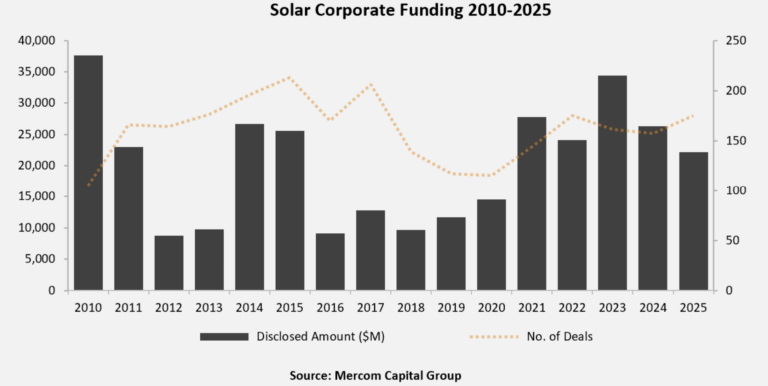

Global corporate funding in the solar sector totaled $22.2 billion across 175 deals in 2025, according to data published by Mercom Capital Group in its 2025 Annual Solar Funding and M&A report.

The total investment figure, encompassing venture capital (VC) funding, public market financing and debt financing, fell by 16% year-on-year for the lowest figure reported since 2020. Deal count however rose 11% year-on-year to 175, reaching a seven-year high.

Debt financing remained the sector’s largest capital source, with $16.1 billion raised across 80 deals in 2025, compared to $18.8 billion in 2024. Of this figure, securitization deals totaled $3.4 billion across nine deals.

Global VC and private equity funding reached $3.5 billion across 75 deals in 2025, down on the $4.5 billion raised last year but covering 15 more deals. Public market financing followed a similar trend, falling to $2.6 billion for its lowest level since 2019 but seeing deal activity increase.

Raj Prabhu, CEO of Mercom Capital Group, commented that deal counts increasing to multi-year highs as total capital raised declined reflects a shift toward smaller and more selective transactions.

“2025 was a year of recalibration for the solar industry, shaped by policy uncertainty, trade and tariff risks, and higher interest rates that weighed on overall funding levels,” he explained. “Policy clarity in the second half of the year helped improve market visibility for investors and supported increased activity in lower-risk, execution-ready deals.”

Prabhu added that another positive takeaway from 2025 was the strength of corporate and project merger and acquisition (M&A) activity. There were 96 corporate M&A transactions in 2025 compared to 82 in 2024 for a 17% year-on-year increase. Solar downstream companies led corporate M&A activity last year, acquiring 72 companies, followed by manufacturers with nine transactions and balance of system companies with five.

Mercom’s report adds that rising electricity demand, in particular from data centres, continued to support downstream activity and utility-scale solar deployment in 2025. The number of large-scale solar project acquisitions last year increased by 13%, with 246 compared to 217 in 2024. The total acquired capacity dropped by 1%, from 37.7 GW in 2024 to 37.4 GW in 2025.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.