Global battery additions reached 108 GW in 2025, according to IEA

Falling costs and greater demand led to a 40% uplift in battery additions in 2025, according to the latest IEA data. This was driven by major acceleration in utility scale deployment, which accounted for 87 GW of the 108 GW added in 2025.

Around 24 GW of utility-scale BESS additions in 2025 were co-located with renewables, on par with the previous year. This means share of capacity for co-located renewables fell just below 30%, which the IEA attributed to market reforms in China in early 2025 which removed broad co-location mandates.

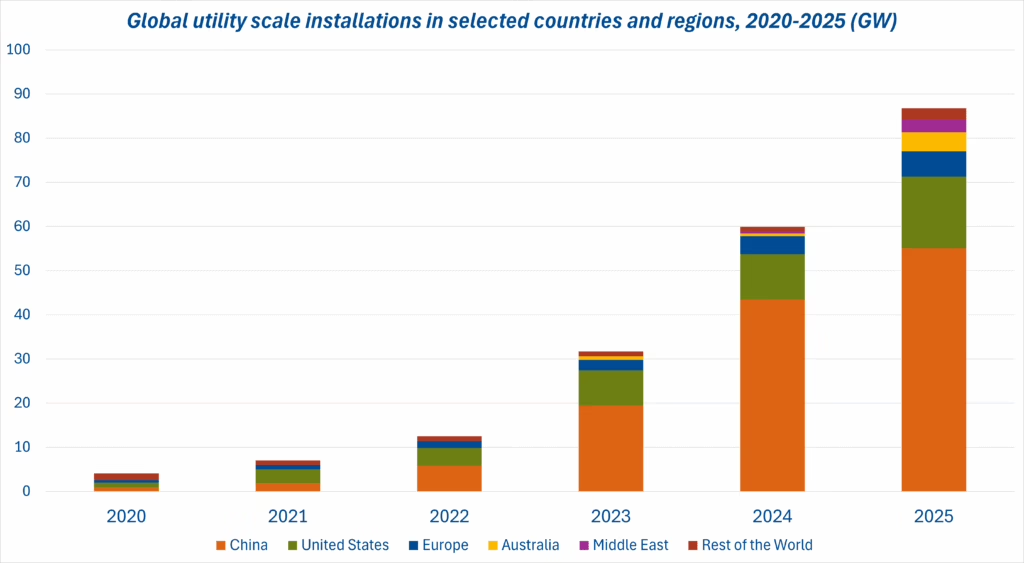

Key growth markets identified by the IEA included Australia, where battery capacity additions surged to nearly 8 GW, almost nine times higher than the previous year.

Utility-scale installations in Australia were up from less than 1 GW in 2024 to around 4.2 GW in 2025, while behind-the-meter additions increased from roughly 0.2 GW to about 3.4 GW, supported by state- and federal-level incentives. It means battery storage now accounts for around 18% of installed dispatchable capacity in Australia, ahead of China (7%), the United States (5%) and Europe (4%).

China continues to dominate BESS additions in absolute terms. Just over 63 GW of new battery capacity was added in China in 2025, one-third more than in 2024. Utility-scale scale installations accounted for 55 GW of the total, with the IEA recording about 8 GW of behind-the-meter additions.

In the United States, 19 GW of battery storage was split across more than 16 GW of utility-scale BESS and nearly 3 GW behind the meter.

Utility-scale BESS may have accounted for lion’s share of new capacity additions but global behind-the-meter installations accelerated also accelerated in 2025. The IEA noted markets with high retail electricity prices and supportive policy frameworks saw increased deployment.

The dramatic fall in costs for battery storage – down by more than 90% between 2010 and 2025 – has supported deployment growth according to the IEA, while the growing proportion of renewables in the global energy generation mix has also increased demand.

IEA noted that early battery projects were concentrated in “lucrative but relatively shallow ancillary service markets” but business models for BESS have changed. Energy arbitrage – storing energy when prices are low, to sell when they are high – has become the dominant application. The IEA estimates the share of projects engaged in this kind of energy shifting has increased from around 40% in 2015 to more than 90% in 2025.

Battery storage durations have also risen as demand for energy shifting has grown. The average duration of projects commissioned rose to three houses in 2025, up from around two hours in 2023.

Please login to comment